Page 375 - CA Final Audit Titanium Full Book. (With Cover Pages)

P. 375

CA Ravi Taori

Director's Authority: The section 21 does not curtail or diminish the Director (Discipline)'s power and

obligation to probe the conduct of a member or firm under any circumstances.

Disciplinary Action: A member may be subjected to disciplinary action under Section 21 of the Chartered

Accountants Act if found guilty of professional or other misconduct.

Professional Misconduct

Definition: Professional misconduct is defined in Part I, II, and III of the First Schedule, and Part I and II of the

Second Schedule.

Compliance: Members engaged in the accountancy profession, whether in practice or service, must adhere to

the provisions in these schedules.

Violation: If a member violates any of the provisions, they will be deemed guilty of professional misconduct.

Other Misconduct

Expectations: Chartered accountants are expected to uphold the highest standards of integrity, both in their

professional and personal lives.

Definition: 'Other misconduct' is defined in part IV of the First Schedule and part III of the Second Schedule.

Authority: The Council has the power to investigate any misconduct by a member, even if it's not related to

their professional work.

Disciplinary Action: Any deviation from these standards, even in non-professional matters, can lead to

disciplinary action. For instance, a member found to have forged a relative's will can face disciplinary action,

even if the forgery wasn't committed professionally.

Convictions: Other Misconduct can also include being convicted by a court for an offense involving moral

turpitude, punishable by transportation or imprisonment. This applies to non-technical offenses committed

professionally by the member (refer to section 8(v) of the Act).

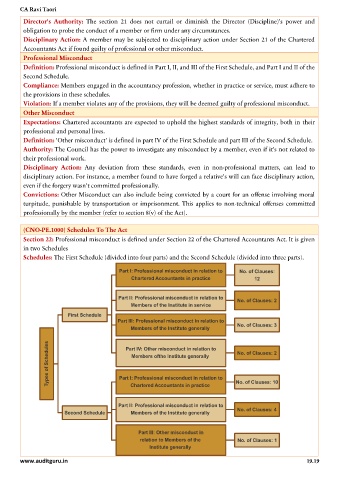

(CNO-PE.1000) Schedules To The Act

Section 22: Professional misconduct is defined under Section 22 of the Chartered Accountants Act. It is given

in two Schedules

Schedules: The First Schedule (divided into four parts) and the Second Schedule (divided into three parts).

www.auditguru.in 19.19