Page 24 - Chapter 9 Registration

P. 24

(I) Legal Provision:

Ü As per section 22 of CGST Act read with Notification No. 10/2019, a supplier who is engaged in

exclusive intra-state supply of goods is liable to be registered in the State/ Union territory from

where he makes a taxable supply, if its aggregate turnover in the financial year exceed ₹ 40 lakh,

subject to some conditions to be fulfilled.

Ü Aggregate turnover includes value of all taxable and exempt supplies under same PAN.

Ü However, as per section 23(1), a person exclusively engaged in making exempt supplies is not

liable to registration

Discussion & Conclusion:

Ü In given case, although the 'aggregate turnover' of Gautam Pvt. Ltd. exceeds threshold limit of ₹ 40

lakh on 30.09.20XX [₹ 55 lakh], it was not required to be registered till 31.10.20XX as it supplied

only exempted goods till that day. However, voluntary registration was allowed u/s 25(3).

Ü Therefore, Gautam Pvt. Ltd. needs to register within 30 days from 01.11.20XX (the date on

which its supplies became taxable) as its turnover had already exceeded the threshold limit of ₹ 40

lakh on 01.11.20XX.

Legal Provision:

(ii)

Ü As per Rule 43(1)(a) of the CGST rule 2017, ITC is disallowed on capital goods used or intended

to be used exclusively for effecting exempt supplies.

Ü However, as per section 18(1)(d) of the CGST Act, where an exempt supply of goods and/or

services by a registered person becomes a taxable supply, such person gets entitled to take credit

of input tax in respect of

Ø inputs held in stock,

Ø inputs contained in semi-finished or finished goods held in stock relatable to such exempt

supply and

Ø on capital goods exclusively used for such exempt supply

on the day immediately preceding the date from which such supply becomes taxable.

Ü Further, Rule 40(1)(a) of the CGST Rules, 2017 lays down that the credit on capital goods can

be claimed after reducing the tax paid on such capital goods by 5% per quarter of a year or part

thereof from the date of the invoice.

Discussion & Conclusion:

Ü In the given case, Gautam Pvt. Ltd. could not claim credit on machinery till the time the supply of

product 'Alpha' for which said machinery was being used was exempt. However, it can claim

credit from 31st October - the day immediately preceding the date from which the supply of

product 'Alpha' became taxable (1st November).

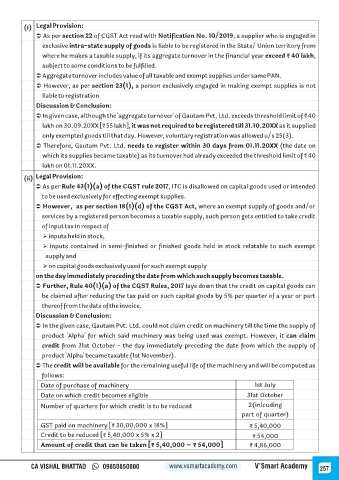

Ü The credit will be available for the remaining useful life of the machinery and will be computed as

follows:

Date of purchase of machinery 1st July

Date on which credit becomes eligible 31st October

Number of quarters for which credit is to be reduced 2(inlcuding

part of quarter)

GST paid on machinery [₹ 30,00,000 x 18%] ₹ 5,40,000

Credit to be reduced [₹ 5,40,000 x 5% x 2] ₹ 54,000

Amount of credit that can be taken [₹ 5,40,000 – ₹ 54,000] ₹ 4,86,000

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 257