Page 9 - CA Final FADU_ChartBook

P. 9

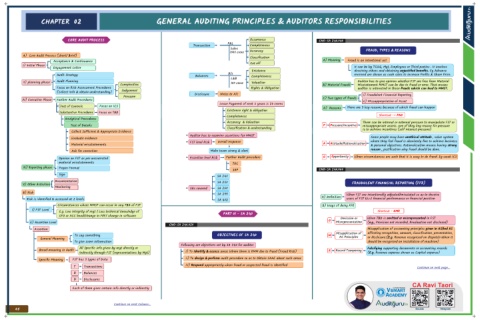

CHAPTER 02 GENERAL AUDITING PRINCIPLES & AUDITORS RESPONSIBILITIES

CORE AUDIT PROCESS Occurrence CNO-SA 240.040

P&L

Transaction Completeness

Sales FRAUD, TYPES & REASONS

1000 crore Accuracy

A) Core Audit Process (short/ Brief)

Classification

Acceptance & Continuance Cut off A) Meaning Fraud is an intentional act

I) Initial Phase

Engagement Letter It can be by TCWG, Mgt, Employees or Third parties . It involves

Existence deceiving others and obtaining unjustified benefits. Eg Advance

B/s

Audit Strategy Balances Completeness received are shown as cash sales to increase Profits & Share Price.

L&B

II) planning phase Audit Planning 100 crore Valuation Auditor has to give opinion whether FST are free from Material

Complexities B) Material Frauds Misstatement MMST can be due to fraud or error. That means

Focus on Risk Assessment Procedures Rights & Obligation auditor is interested in those frauds which can lead to MMST.

Judgement

(Collect info & obtain understanding)

Disclosure Notes to A/c i) Fraudulent Financial Reporting

Pressure C) Two types of frauds

III) Execution Phase Further Audit Procedures ii) Missappropriation of Asset

Lease Payment of next 5 years is 20 crores

Test of Controls Focus on ICS D) Reasons There are 3 key reasons because of which fraud can happen

Existence right & obligation

Substantive Procedures Focus on TBD

Completeness Shortcut -> PAO

Analytical Procedures

Accuracy & Valuation There can be internal or external pressure to manipulate FST or

Test of Details P Pressure/Incentive missappropriate assets. one of they key reason for pressure

Classification & understanding is to achieve incentives (self interest pressure)

Collect Sufficient & Appropriate Evidence

Auditor has to examine assertions far MMST

Evaluate evidence Some people may have unethical attitude , value system

FST level Risk overall response where they feel fraud is absolutely fine to achieve business

Material misstatements A Attitude/Rationalisation & personal objectives. Rationalisation means having strong

reason , justification why fraud should be done.

Ask for correction Make team strong & alert

Opinion on FST as per uncorrected Assertion level Risk Further Audit procedure O Opportunity When circumstances are such that it is easy to do fraud. Eg weak ICS

material misstatements TOC

IV) Reporting phase Proper Format

SAP CNO-SA 240.060

Sign

SA 240

Documentation SA 250 FRAUDULENT FINANCIAL REPORTING (FFR)

V) Other Activities

Monitoring

SAs covered SA 260

B) Risk

SA 299 When FST are intentionally adjusted/misstated so as to deceive

A) Definition

Risk is identified & assessed at 2 levels SA 402 users of FST W.r.t financial performance or financial position

Circumstances where MMST can occur in any TBD of FST B) Ways of doing FFR

I) FST Level

E.g. Low Integrity of mgt / Low technical knowledge of PART 01 - SA 240 Shortcut - OMR

CFO or ACC head/change in FRF/ change in software

Omission or When TBD is omitted or misrepresented in FST

O

ii) Assertion Level Misrepresentation (e.g., Provision not recorded, Revaluation not disclosed)

CNO-SA 240.020

Assertion Misapplication of accounting principles given in AS/Ind AS

Misapplication of affecting recognition, amount, classification, presentation,

To say something OBJECTIVES OF SA 240 M

General Meaning AC Principles or disclosure.(E.g. Revenue recognised on dispatch When it

To give some information should be recognised on installation of machine)

Following are objectives set by SA 240 for auditor

All Specific info given by mgt directly or Falsifying supporting documents or accounting records

Broad meaning in Audit R Record Tampering

indirectly through FST (representations by Mgt) I) To identify & assess areas Where there is RMM due to fraud (Fraud Risk) (E.g. Revenue expense shown as Capital expense)

ii) To design & perform audit procedure so as to Obtain SAAE about such areas

Specific Meaning FST has 3 types of Data

iii) Respond appropriately when fraud or suspected fraud is identified

T Transactions Continue on next page...

B Balances

D Disclosures

Each of them gives certain info directly or indirectly

Continue on next Column...

05