Page 12 - Ch_10 ITC

P. 12

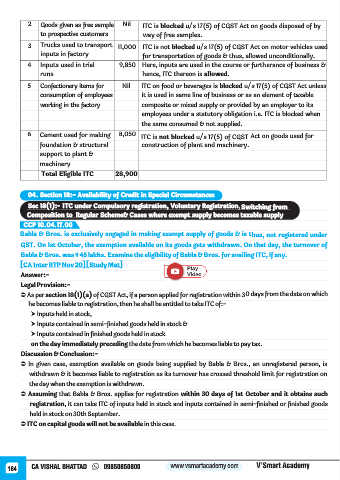

2 Goods given as free sample Nil ITC is blocked u/s 17(5) of CGST Act on goods disposed of by

to prospective customers way of free samples.

3 Trucks used to transport 11,000 ITC is not blocked u/s 17(5) of CGST Act on motor vehicles used

inputs in factory for transportation of goods & thus, allowed unconditionally.

4 Inputs used in trial 9,850 Here, inputs are used in the course or furtherance of business &

runs hence, ITC thereon is allowed.

5 Confectionery items for Nil ITC on food or beverages is blocked u/s 17(5) of CGST Act unless

consumption of employees it is used in same line of business or as an element of taxable

working in the factory composite or mixed supply or provided by an employer to its

employees under a statutory obligation i.e. ITC is blocked when

the same consumed & not supplied.

6 Cement used for making 8,050 ITC is not blocked u/s 17(5) of CGST Act on goods used for

foundation & structural construction of plant and machinery.

support to plant &

machinery

Total Eligible ITC 28,900

04. Section 18:- Availability of Credit in Special Circumstances

Sec 18(1):- ITC under Compulsory registration, Voluntary Registration, Switching from

Composition to Regular Scheme& Cases where exempt supply becomes taxable supply

CCP 10.04.17.00

Babla & Bros. is exclusively engaged in making exempt supply of goods & is thus, not registered under

GST. On 1st October, the exemption available on its goods gets withdrawn. On that day, the turnover of

Babla & Bros. was ₹ 45 lakhs. Examine the eligibility of Babla & Bros. for availing ITC, if any.

[CA Inter RTP Nov 20] [Study Mat]

Answer:-

Legal Provision:-

Ü As per section 18(1)(a) of CGST Act, if a person applied for registration within 30 days from the date on which

he becomes liable to registration, then he shall be entitled to take ITC of:-

† Inputs held in stock,

† Inputs contained in semi-finished goods held in stock &

† Inputs contained in finished goods held in stock

on the day immediately preceding the date from which he becomes liable to pay tax.

Discussion & Conclusion:-

Ü In given case, exemption available on goods being supplied by Babla & Bros., an unregistered person, is

withdrawn & it becomes liable to registration as its turnover has crossed threshold limit for registration on

the day when the exemption is withdrawn.

Ü Assuming that Babla & Bros. applies for registration within 30 days of 1st October and it obtains such

registration, it can take ITC of inputs held in stock and inputs contained in semi-finished or finished goods

held in stock on 30th September.

Ü ITC on capital goods will not be available in this case.

164 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy