Page 14 - Ch2_Supply

P. 14

Brief notes should form part of your answer for treatment of items in Sl. No. (i) to (v).

[CA Inter Nov 22 Exam]

Answer:-

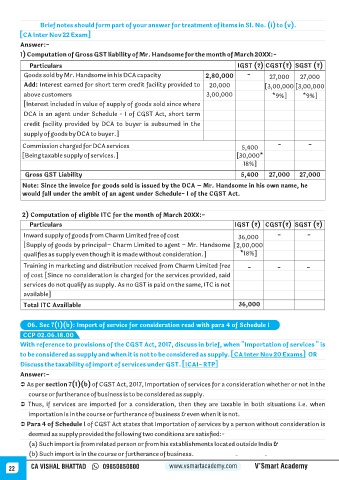

1) Computation of Gross GST liability of Mr. Handsome for the month of March 20XX:-

Particulars IGST (₹) CGST(₹) SGST (₹)

Goods sold by Mr. Handsome in his DCA capacity 2,80,000 - 27,000 27,000

Add: Interest earned for short term credit facility provided to 20,000 [3,00,000 [3,00,000

above customers 3,00,000 *9%] *9%]

[Interest included in value of supply of goods sold since where

DCA is an agent under Schedule - I of CGST Act, short term

credit facility provided by DCA to buyer is subsumed in the

supply of goods by DCA to buyer.]

Commission charged for DCA services 5,400 - -

[Being taxable supply of services.] [30,000*

18%]

Gross GST Liability 5,400 27,000 27,000

Note: Since the invoice for goods sold is issued by the DCA – Mr. Handsome in his own name, he

would fall under the ambit of an agent under Schedule- I of the CGST Act.

2) Computation of eligible ITC for the month of March 20XX:-

Particulars IGST (₹) CGST(₹) SGST (₹)

Inward supply of goods from Charm Limited free of cost 36,000 - -

[Supply of goods by principal– Charm Limited to agent – Mr. Handsome [2,00,000

qualifies as supply even though it is made without consideration.] *18%]

Training in marketing and distribution received from Charm Limited free - - -

of cost [Since no consideration is charged for the services provided, said

services do not qualify as supply. As no GST is paid on the same, ITC is not

available]

Total ITC Availlable 36,000

06. Sec 7(1)(b): Import of service for consideration read with para 4 of Schedule I

CCP 02.06.18.00

With reference to provisions of the CGST Act, 2017, discuss in brief, when "Importation of services " is

to be considered as supply and when it is not to be considered as supply. [CA Inter Nov 20 Exams] OR

Discuss the taxability of import of services under GST. [ICAI- RTP]

Answer:-

Ü As per section 7(1)(b) of CGST Act, 2017, Importation of services for a consideration whether or not in the

course or furtherance of business is to be considered as supply.

Ü Thus, if services are imported for a consideration, then they are taxable in both situations i.e. when

importation is in the course or furtherance of business & even when it is not.

Ü Para 4 of Schedule I of CGST Act states that Importation of services by a person without consideration is

deemed as supply provided the following two conditions are satisfied:-

(a) Such import is from related person or from his establishments located outside India &

(b) Such import is in the course or furtherance of business. - -

22 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy