Page 215 - CA Inter Audit PARAM

P. 215

CA Ravi Taori

During the year 2022-23, services of an employee of company were terminated. The said employee had

filed a suit against the company in respect of certain compensation dues amounting to ₹ 10 lakhs which

were not paid to him. Based upon advice of legal counsel, the company had made a provision of ₹ 10 lacs

in financial statements for year 2022-23. However, somewhere in June 2023, there is an out of court

settlement between company and employee for ₹ 6 lakhs. The statutory audit of company is under

progress and audit report has not yet been finalized. How internal auditor should have proceeded in

situation?

Answer Subsequent events are events occurring between the date of financial statements and the date of the

auditor’s report and facts that become known to the auditor after the date of the auditor’s report.

In the given case, the company had already made provision of ₹ 10 lakhs in financial statements for year

2022-23. However, there is an out of court settlement between the company and employee for ₹ 6 lakhs.

It is an example of event which provides evidence of conditions that existed at the date of financial

st

statements i.e. 31 March, 2023. It provides evidence on adjustment in provision amount already made in

financial statements. Therefore, internal auditor should ask management to revise provision downwards

to ₹ 6 lakhs so that financial statements are in accordance with applicable accounting standards.

Authors Note -- Question is asked from point of view of Internal Auditor, as SAs are not applicable while

performing Internal Audit Don’t give reference of SA 560

Auditor Responsibility - Events occurring between the date Old Course -- (P16M/ M16R/N17R/N19M/

QNO of the financial statements and the date of the auditor’s M19R/M21E)

560.03

report Bhaskar CNO- SA560.060 New Course – (M24R)

The auditor shall perform audit procedures designed to obtain sufficient appropriate audit evidence that

all events occurring between the date of the financial statements and the date of the auditor’s report that

require adjustment of, or disclosure in, the financial statements have been identified. Explain.

OR

Indicate briefly the procedures to identify subsequent events requiring adjustment of or disclosure in the

financial statements.

OR

The auditors should consider the effect of subsequent events on the financial statement and on auditor’s

report– Comment according to SA 560.

OR

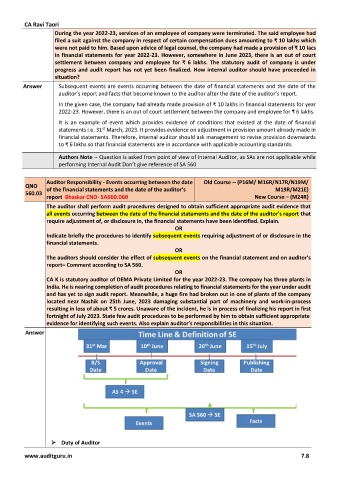

CA K is statutory auditor of DEMA Private Limited for the year 2022-23. The company has three plants in

India. He is nearing completion of audit procedures relating to financial statements for the year under audit

and has yet to sign audit report. Meanwhile, a huge fire had broken out in one of plants of the company

located near Nashik on 25th June, 2023 damaging substantial part of machinery and work-in-process

resulting in loss of about ₹ 5 crores. Unaware of the incident, he is in process of finalizing his report in first

fortnight of July 2023. State few audit procedures to be performed by him to obtain sufficient appropriate

evidence for identifying such events. Also explain auditor’s responsibilities in this situation.

Answer

➢ Duty of Auditor

www.auditguru.in 7.8