Page 24 - CA Inter Audit PARAM

P. 24

CA Ravi Taori

QNO-- Case Study on Professional Skepticism New Course – (S24M)

200.35 Bhaskar CNO – SA 200.120

"Truthful Products Private Limited is engaged in trading stationery items. During the year 2023-24, there was

a huge fire in one storage location of the company resulting in loss of inventories of ₹ 5 crores. As a result,

the operations of the company were badly affected for about two months. Unfortunately, the insurance

claim of the company was rejected due to certain defects in the policy issued and loss was booked by

company in the year 2023-24 itself. There was no change in nature of business of company in relation to the

last year. The draft financial statements of the company reflect following information:

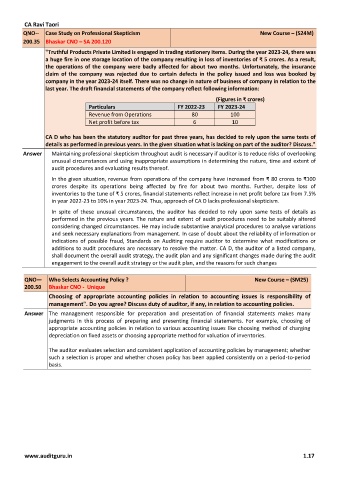

(Figures in ₹ crores)

Particulars FY 2022-23 FY 2023-24

Revenue from Operations 80 100

Net profit before tax 6 10

CA D who has been the statutory auditor for past three years, has decided to rely upon the same tests of

details as performed in previous years. In the given situation what is lacking on part of the auditor? Discuss."

Answer Maintaining professional skepticism throughout audit is necessary if auditor is to reduce risks of overlooking

unusual circumstances and using inappropriate assumptions in determining the nature, time and extent of

audit procedures and evaluating results thereof.

In the given situation, revenue from operations of the company have increased from ₹ 80 crores to ₹100

crores despite its operations being affected by fire for about two months. Further, despite loss of

inventories to the tune of ₹ 5 crores, financial statements reflect increase in net profit before tax from 7.5%

in year 2022-23 to 10% in year 2023-24. Thus, approach of CA D lacks professional skepticism.

In spite of these unusual circumstances, the auditor has decided to rely upon same tests of details as

performed in the previous years. The nature and extent of audit procedures need to be suitably altered

considering changed circumstances. He may include substantive analytical procedures to analyse variations

and seek necessary explanations from management. In case of doubt about the reliability of information or

indications of possible fraud, Standards on Auditing require auditor to determine what modifications or

additions to audit procedures are necessary to resolve the matter. CA D, the auditor of a listed company,

shall document the overall audit strategy, the audit plan and any significant changes made during the audit

engagement to the overall audit strategy or the audit plan, and the reasons for such changes

QNO— Who Selects Accounting Policy ? New Course – (SM25)

200.50 Bhaskar CNO - Unique

Choosing of appropriate accounting policies in relation to accounting issues is responsibility of

management". Do you agree? Discuss duty of auditor, if any, in relation to accounting policies.

Answer The management responsible for preparation and presentation of financial statements makes many

judgments in this process of preparing and presenting financial statements. For example, choosing of

appropriate accounting policies in relation to various accounting issues like choosing method of charging

depreciation on fixed assets or choosing appropriate method for valuation of inventories.

The auditor evaluates selection and consistent application of accounting policies by management; whether

such a selection is proper and whether chosen policy has been applied consistently on a period-to-period

basis.

www.auditguru.in 1.17