Page 273 - CA Inter Audit PARAM

P. 273

CA Ravi Taori

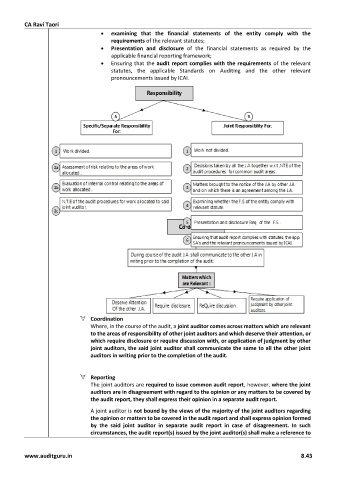

• examining that the financial statements of the entity comply with the

requirements of the relevant statutes;

• Presentation and disclosure of the financial statements as required by the

applicable financial reporting framework;

• Ensuring that the audit report complies with the requirements of the relevant

statutes, the applicable Standards on Auditing and the other relevant

pronouncements issued by ICAI.

Coordination

Where, in the course of the audit, a joint auditor comes across matters which are relevant

to the areas of responsibility of other joint auditors and which deserve their attention, or

which require disclosure or require discussion with, or application of judgment by other

joint auditors, the said joint auditor shall communicate the same to all the other joint

auditors in writing prior to the completion of the audit.

Reporting

The joint auditors are required to issue common audit report, however, where the joint

auditors are in disagreement with regard to the opinion or any matters to be covered by

the audit report, they shall express their opinion in a separate audit report.

A joint auditor is not bound by the views of the majority of the joint auditors regarding

the opinion or matters to be covered in the audit report and shall express opinion formed

by the said joint auditor in separate audit report in case of disagreement. In such

circumstances, the audit report(s) issued by the joint auditor(s) shall make a reference to

www.auditguru.in 8.43