Page 333 - CA Inter Audit PARAM

P. 333

CA Ravi Taori

matter to the Central Government within such time and in such manner as may be

prescribed.

It must be noted that auditor is not expected to consider each and every transaction but to

evaluate the system as a whole. Therefore, if the auditor while performing normal duties

comes across any instance, he/she should report the matter to the RBI in addition to

Chairman/Managing Director/Chief Executive of the concerned bank.

QNO Additional Reports apart from report on financial statements Old Course-- (M21R)

BA.24 #Unique

Your firm of auditors, SRG & Co., has been appointed as Statutory Central Auditors of Reliable Bank. Explain

the reporting requirements of the Statutory Central Auditors (SCAs) in addition to their main audit report.

Answer Presently, the Statutory Central Auditors (SCAs) have to furnish the following reports in addition to

their main audit report:

a. Report on adequacy and operating effectiveness of Internal Controls over Financial Reporting in

case of banks which are registered as companies under the Companies Act in terms of Section

143(3)(i) of the Companies Act, 2013 which is normally to be given as an Annexure to the main

audit report as per the Guidance Note on Audit of Internal Financial Controls over Financial

Reporting issued by the ICAI.

b. Long Form Audit Report. (LFAR)

c. Report on compliance with SLR requirements.

d. Report on whether the treasury operations of the bank have been conducted in accordance with

the instructions issued by the RBI from time to time.

e. Report on whether the income recognition, asset classification and provisioning have been made

as per the guidelines issued by the RBI from time to time.

f. Report on whether any serious irregularity was noticed in the working of the bank which requires

immediate attention.

g. Report on status of the compliance by the bank with regard to the implementation of

recommendations of the Ghosh Committee relating to frauds and malpractices and of the

recommendations of Jilani Committee on internal control and inspection/credit system.

h. Report on instances of adverse credit-deposit ratio in the rural areas.

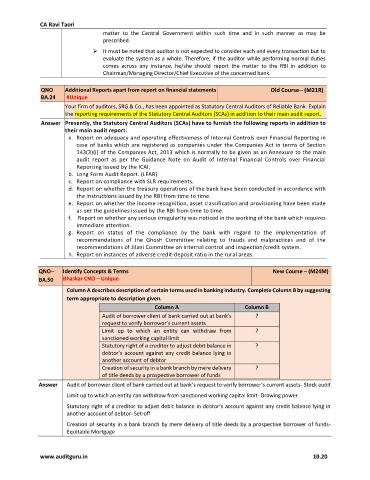

QNO-- Identify Concepts & Terms New Course – (M24M)

BA.50 Bhaskar CNO – Unique

Column A describes description of certain terms used in banking industry. Complete Column B by suggesting

term appropriate to description given.

Column A Column B

Audit of borrower client of bank carried out at bank’s ?

request to verify borrower’s current assets

Limit up to which an entity can withdraw from ?

sanctioned working capital limit

Statutory right of a creditor to adjust debit balance in ?

debtor’s account against any credit balance lying in

another account of debtor

Creation of security in a bank branch by mere delivery ?

of title deeds by a prospective borrower of funds

Answer Audit of borrower client of bank carried out at bank’s request to verify borrower’s current assets- Stock audit

Limit up to which an entity can withdraw from sanctioned working capital limit- Drawing power

Statutory right of a creditor to adjust debit balance in debtor’s account against any credit balance lying in

another account of debtor- Set-off

Creation of security in a bank branch by mere delivery of title deeds by a prospective borrower of funds-

Equitable Mortgage

www.auditguru.in 10.20