Page 215 - CA Inter Bhaskar Vol 1

P. 215

CA RAVI TAORI recovery of credit sales without any authorization. Article failed to point it out as irregularity as all

AUDIT EVIDENCE

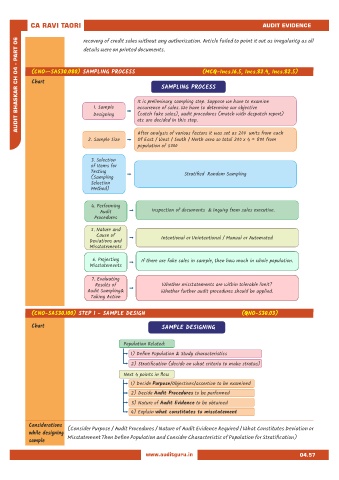

AUDIT BHASKAR CH 04 - PART 06 AUDIT BHASKAR CHAPTER 07 (CNO—SA530.080) SAMPLING PROCESS (MCQ-Incs.16.5, Incs.82.4, Incs.82.5)

details were on printed documents.

Chart

SAMPLING PROCESS

It is preliminary sampling step. Suppose we have to examine

1. Sample

occurrence of sales. We have to determine our objective

(catch fake sales), audit procedures (match with despatch report)

Designing

etc are decided in this step.

Of East / West / South / North area so total 200 x 4 = 800 from

2. Sample Size

population of 5000

3. Selection After analysis of various factors it was set as 200 units from each

of Items for

Testing Stratified Random Sampling

(Sampling

Selection

Method)

4. Performing

Audit Inspection of documents & Inquiry from sales executive.

Procedures

5. Nature and

Cause of Intentional or Unintentional / Manual or Automated

Deviations and

Misstatements

6. Projecting If there are fake sales in sample, then how much in whole population.

Misstatements

7. Evaluating

Results of Whether misstatements are within tolerable limit?

Audit Sampling& Whether further audit procedures should be applied.

Taking Action

(CNO-SA530.100) STEP 1 - SAMPLE DESIGN (QNO-530.03)

Chart SAMPLE DESIGNING

Population Related:

1) Define Population & Study characteristics

2) Stratification (decide on what criteria to make stratas)

Next 4 points in flow

1) Decide Purpose/Objectives/assertion to be examined

2) Decide Audit Procedures to be performed

3) Nature of Audit Evidence to be obtained

4) Explain what constitutes to misstatement

Considerations

(Consider Purpose / Audit Procedures / Nature of Audit Evidence Required / What Constitutes Deviation or

while designing

Misstatement Then Define Population and Consider Characteristic of Population for Stratification)

sample

www.auditguru.in 04.57