Page 15 - 1. COMPILER QB - INDAS 1

P. 15

subsequently when the meeting was held it was ratified by the shareholders.

Issue 5: The company had acquired intangible assets as trademarks amounting to Rs. 2,50,000. The company

assumes to have indefinite life of these assets. The fair value of the intangible assets as on the date of

transition was Rs. 3,00,000. However, the company wants to carry the intangible assets at Rs. 2,50,000 only.

Issue 6: After consideration of possible effects as per Ind AS, the deferred tax impact is computed as Rs.

25,000. This amount will further increase the portion of deferred tax liability. There is no requirement to carry

out the separate calculation of deferred tax on account of Ind AS adjustment.

Management wants to know the impact of Ind AS in the financial statements of company for its general

understanding. Prepare Ind AS Impact Analysis Report (Extract) for HIM Limited for presentation to the

management wherein you are required to discuss the corresponding differences between Earlier IGAAP (AS)

and Ind AS against each identified issue for preparation of transition date balance sheet. Also pass journal

entry for each issue.

SOLUTION

1. Preliminary Impact Assessment on Transition to Transition to Ind AS in HIM Limited’s Financial

Statements

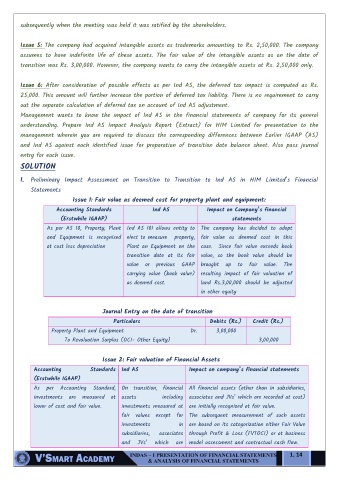

Issue 1: Fair value as deemed cost for property plant and equipment:

Accounting Standards Ind AS Impact on Company’s financial

(Erstwhile IGAAP) statements

As per AS 10, Property, Plant Ind AS 101 allows entity to The company has decided to adopt

and Equipment is recognised elect to measure property, fair value as deemed cost in this

at cost less depreciation Plant an Equipment on the case. Since fair value exceeds book

transition date at its fair value, so the book value should be

value or previous GAAP brought up to fair value. The

carrying value (book value) resulting impact of fair valuation of

as deemed cost. land Rs.3,00,000 should be adjusted

in other equity

Journal Entry on the date of transition

Particulars Debits (Rs.) Credit (Rs.)

Property Plant and Equipment Dr. 3,00,000

To Revaluation Surplus (OCI- Other Equity) 3,00,000

Issue 2: Fair valuation of Financial Assets

Accounting Standards Ind AS Impact on company’s financial statements

(Erstwhile IGAAP)

As per Accounting Standard, On transition, financial All financial assets (other than in subsidiaries,

investments are measured at assets including associates and JVs’ which are recorded at cost)

lower of cost and fair value. investments measured at are initially recognized at fair value.

fair values except for The subsequent measurement of such assets

investments in are based on its categorization either Fair Value

subsidiaries, associates through Profit & Loss (FVTOCI) or at business

and JVs’ which are model assessment and contractual cash flow.

1. 14