Page 11 - 9. COMPILER QB - INDAS 23

P. 11

NEWLY ADDED QUESTIONS IN ICAI MODULE FOR MAY 22 ONWARDS

Question 9: (Same Question was asked in RTP May 21)- Same as Q.4.

How will you capitalise the interest when qualifying assets are funded by borrowings in the nature of bonds

that are issued at discount?

Y Ltd. issued at the start of year 1, 10% (interest paid annually and having maturity period of 4 years) bonds

with a face value of Rs 2,00,000 at a discount of 10% to finance a qualifying asset which is ready for intended

use at the end of year 2.

Compute the amount of borrowing costs to be capitalized if the company amortizes discount using Effective

Interest Rate method by applying 13.39% p.a. of EIR.

Solution:

Capitalisation Method

As per the Standard, borrowing costs may include interest expense calculated using the effective interest

method. Further, capitalisation of borrowing cost should cease where substantially all the activities necessary to

prepare the qualifying asset for its intended use or sale are complete.

Thus, only that portion of the amortized discount should be capitalised as part of the cost of a qualifying asset

which relates to the period during which acquisition, construction or production of the asset takes place.

Capitalisation of Interest

Hence based on the above explanation the amount of borrowing cost of year 1 & 2 are to be capitalised and

the borrowing cost relating to year 3 & 4 should be expensed.

Quantum of Borrowing

The value of the bond to Y Ltd. is the transaction price i.e. Rs 1,80,000 (2,00,000 – 20,000) Therefore, Y Ltd

will recognize the borrowing at Rs 1,80,000.

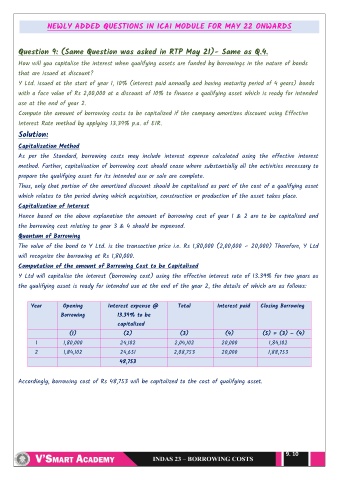

Computation of the amount of Borrowing Cost to be Capitalised

Y Ltd will capitalise the interest (borrowing cost) using the effective interest rate of 13.39% for two years as

the qualifying asset is ready for intended use at the end of the year 2, the details of which are as follows:

Year Opening Interest expense @ Total Interest paid Closing Borrowing

Borrowing 13.39% to be

capitalised

(1) (2) (3) (4) (5) = (3) – (4)

1 1,80,000 24,102 2,04,102 20,000 1,84,102

2 1,84,102 24,651 2,08,753 20,000 1,88,753

48,753

Accordingly, borrowing cost of Rs 48,753 will be capitalized to the cost of qualifying asset.

9. 10