Page 7 - 9. COMPILER QB - INDAS 23

P. 7

Q5 (RTP Nov. 21)

Nikka Limited has obtained a term loan of Rs. 620 lacs for a complete renovation and modernisation of its

Factory on 1st April, 20X1. Plant and Machinery was acquired under the modernisation scheme and

installation was completed on 30th April, 20X2. An expenditure of Rs. 510 lacs was incurred on installation

of Plant and Machinery, Rs. 54 lacs has been advanced to suppliers for additional assets (acquired on 25th

April, 20X1) which were also installed on 30th April, 20X2 and the balance loan of Rs. 56 lacs has been

used for working capital purposes. Management of Nikka Limited considers the 12 months period as a

substantial period of time to get the asset ready for its intended use.

The company has paid total interest of Rs. 68.20 lacs during financial year 20X1-20X2 on the above loan.

The accountant seeks your advice on how to account for the interest paid in the books of accounts. Will

th

your answer be different, if the whole process of renovation and modernization gets completed by 28

February, 20X2?

Solution

As per Ind AS 23, Borrowing costs that are directly attributable to the acquisition, construction or

production of a qualifying asset form part of the cost of that asset. Other borrowing costs are recognised as

an expense.

Where, a qualifying asset is an asset that necessarily takes a substantial period of time to get ready for its

intended use or sale.

Accordingly, the treatment of Interest of Rs. 68.20 lacs occurred during the year 20X1-20X2 would be as

follows:

(i) When construction of asset completed on 30th April, 20X2

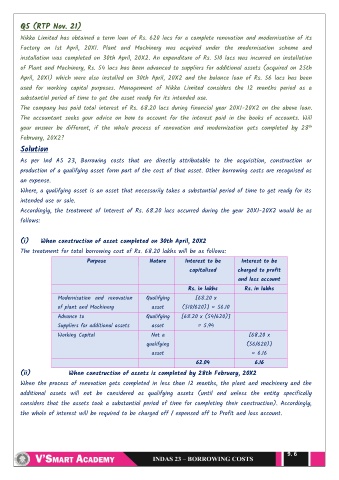

The treatment for total borrowing cost of Rs. 68.20 lakhs will be as follows:

Purpose Nature Interest to be Interest to be

capitalised charged to profit

and loss account

Rs. in lakhs Rs. in lakhs

Modernisation and renovation Qualifying [68.20 x

of plant and Machinery asset (510/620)] = 56.10

Advance to Qualifying [68.20 x (54/620)]

Suppliers for additional assets asset = 5.94

Working Capital Not a [68.20 x

qualifying (56/620)]

asset = 6.16

62.04 6.16

(ii) When construction of assets is completed by 28th February, 20X2

When the process of renovation gets completed in less than 12 months, the plant and machinery and the

additional assets will not be considered as qualifying assets (until and unless the entity specifically

considers that the assets took a substantial period of time for completing their construction). Accordingly,

the whole of interest will be required to be charged off / expensed off to Profit and loss account.

9. 6