Page 4 - 28. COMPILER QB - IND AS 8

P. 4

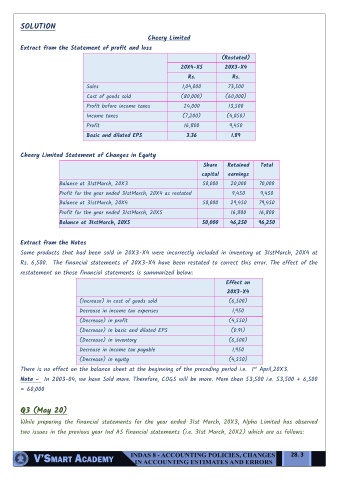

SOLUTION

Cheery Limited

Extract from the Statement of profit and loss

(Restated)

20X4-X5 20X3-X4

Rs. Rs.

Sales 1,04,000 73,500

Cost of goods sold (80,000) (60,000)

Profit before income taxes 24,000 13,500

Income taxes (7,200) (4,050)

Profit 16,800 9,450

Basic and diluted EPS 3.36 1.89

Cheery Limited Statement of Changes in Equity

Share Retained Total

capital earnings

Balance at 31stMarch, 20X3 50,000 20,000 70,000

Profit for the year ended 31stMarch, 20X4 as restated 9,450 9,450

Balance at 31stMarch, 20X4 50,000 29,450 79,450

Profit for the year ended 31stMarch, 20X5 16,800 16,800

Balance at 31stMarch, 20X5 50,000 46,250 96,250

Extract from the Notes

Some products that had been sold in 20X3-X4 were incorrectly included in inventory at 31stMarch, 20X4 at

Rs. 6,500. The financial statements of 20X3-X4 have been restated to correct this error. The effect of the

restatement on those financial statements is summarized below:

Effect on

20X3-X4

(Increase) in cost of goods sold (6,500)

Decrease in income tax expenses 1,950

(Decrease) in profit (4,550)

(Decrease) in basic and diluted EPS (0.91)

(Decrease) in inventory (6,500)

Decrease in income tax payable 1,950

(Decrease) in equity (4,550)

st

There is no effect on the balance sheet at the beginning of the preceding period i.e. 1 April,20X3.

Note - In 2003-04, we have Sold more. Therefore, COGS will be more. More than 53,500 i.e. 53,500 + 6,500

= 60,000

Q3 (May 20)

While preparing the financial statements for the year ended 31st March, 20X3, Alpha Limited has observed

two issues in the previous year Ind AS financial statements (i.e. 31st March, 20X2) which are as follows:

28. 3