Page 391 - CA Final PARAM Digital Book.

P. 391

First Schedule, Part I,Cl,6 Solicitation Old Course – (M06E, N10R, M12R, M12M, M13R, M14R, PM17,

QNO (Tender) Land Revenue SM17, N18M, N20E)

681.000

TITANIUM CNO – PE.1140 New Course – (SM23)

M/s LMN, a firm of Chartered Accountants responded to a tender from a State Government for

computerization of land revenue records. For this purpose, the firm also paid ` 50,000 as earnest

deposit as part of the terms of the tender.

Answer Part I -- Relevant Laws

▪ Clause (6) of Part I of First Schedule to the Chartered Accountants Act, 1949

Part II -- Requirements of Relevant Laws

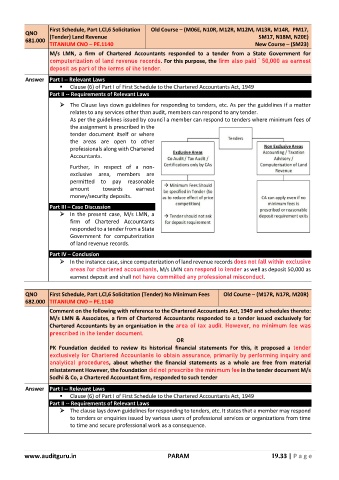

➢ The Clause lays down guidelines for responding to tenders, etc. As per the guidelines if a matter

relates to any services other than audit, members can respond to any tender.

As per the guidelines issued by council a member can respond to tenders where minimum fees of

the assignment is prescribed in the

tender document itself or where

the areas are open to other

professionals along with Chartered

Accountants.

Further, in respect of a non-

exclusive area, members are

permitted to pay reasonable

amount towards earnest

money/security deposits.

Part III – Case Discussion

➢ In the present case, M/s LMN, a

firm of Chartered Accountants

responded to a tender from a State

Government for computerization

of land revenue records.

Part IV – Conclusion

➢ In the instance case, since computerization of land revenue records does not fall within exclusive

areas for chartered accountants, M/s LMN can respond to tender as well as deposit 50,000 as

earnest deposit and shall not have committed any professional misconduct.

QNO First Schedule, Part I,Cl,6 Solicitation (Tender) No Minimum Fees Old Course – (M17R, N17R, M20R)

682.000 TITANIUM CNO – PE.1140

Comment on the following with reference to the Chartered Accountants Act, 1949 and schedules thereto:

M/s LMN & Associates, a firm of Chartered Accountants responded to a tender issued exclusively for

Chartered Accountants by an organisation in the area of tax audit. However, no minimum fee was

prescribed in the tender document.

OR

PK Foundation decided to review its historical financial statements For this, it proposed a tender

exclusively for Chartered Accountants to obtain assurance, primarily by performing inquiry and

analytical procedures, about whether the financial statements as a whole are free from material

misstatement However, the foundation did not prescribe the minimum fee in the tender document M/s

Sodhi & Co, a Chartered Accountant firm, responded to such tender

Answer Part I -- Relevant Laws

▪ Clause (6) of Part I of First Schedule to the Chartered Accountants Act, 1949

Part II -- Requirements of Relevant Laws

➢ The clause lays down guidelines for responding to tenders, etc. It states that a member may respond

to tenders or enquiries issued by various users of professional services or organizations from time

to time and secure professional work as a consequence.

www.auditguru.in PARAM 19.33 | P a g e