Page 40 - CA Final PARAM Digital Book.

P. 40

Responsibility of Joint Auditors & Old Course – (N04E, M15R, N15E, SM17, PM17, N17M, M18M,

QNO Difference of opinion amongst Joint N18E, N18M, N19E, SM21)

28.100 Auditor New Course (SM23)

TITANIUM CNO - SA299.100 / SA299.080

KRP Ltd., at its annual general meeting, appointed Mr. X, Mr. Y and Mr. Z as joint auditors to conduct

auditing for the financial year 2015-16. For the valuation of gratuity scheme of the company, Mr. X, Mr. Y

and Mr. Z wanted to refer their own known Actuaries.

Due to difference of opinion, all the joint auditors consulted their respective Actuaries. Subsequently, major

difference was found in the actuary reports. However, Mr. X agreed to Mr. Y’s actuary report, though, Mr. Z

did not. Mr. X contends that Mr. Y’s actuary report shall be considered in audit report due to majority of

votes. Now, Mr. Z is in dilemma.

You are required to briefly explain the responsibilities of auditors when they are jointly and severally

responsible in respect of audit conducted by them and also guide Mr. Z in such situation.

OR

Excellent Bank Ltd. is a Public Limited Company.. The Bank appoints 3 Joint Auditors for the financial year

ending 31/03/2019. All the 3 Joint Auditors divide the work with mutual consent. Verification of

Consolidation, however, remained undivided.

All branches and zones were divided amongst the 3 Joint Auditors" During audit of zones, CA. Z, one of the

joint auditors expressed a concern about internal control in one of the large corporate branches situated in

his zone.

The irregularity was net reported, in the final accounts as the other 2 Joint Auditors were not in favour of

reporting and decision of not reporting the same was taken on the basis of majority. Subsequently, fraud

has been detected in the said branch which was audited by CA. Z.

Bank seeks your advice about the responsibility of the 3 Joint Auditors in the above situation.

Answer Part I -- Relevant Standards & Laws

▪ SA 299 on, “Responsibility of Joint Auditors”

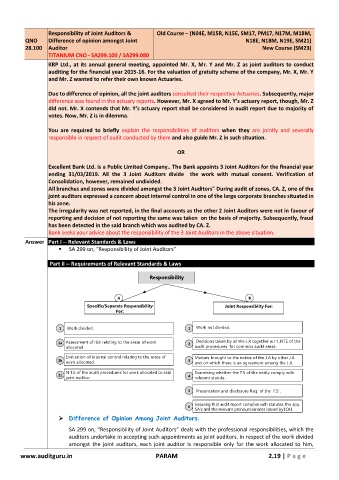

Part II -- Requirements of Relevant Standards & Laws

Responsibility

A A B B

Specific/Separate Responsibility Joint Responsiblity For:

For:

1 Work divided. 1 Work not divided.

2a Assessment of risk relating to the areas of work 2 Decisions taken by all the J.A together w.r.t ,NTE of the

allocated . audit procedures for common audit areas .

Evaluation of internal control relating to the areas of Matters brought to the notice of the J.A by other J.A

2b work allocated . 3 and on which there is an agreement among the J.A.

N.T.E of the audit procedures for work allocated to said Examining whether the F.S of the entity comply with

2c 4

joint auditor. relevant statute.

5 Presentation and disclosure Req of the F.S .

Ensuring that audit report complies with statutes, the app.

6 SA s and the relevant pronouncements issued by ICAI.

➢ Difference of Opinion Among Joint Auditors:

SA 299 on, “Responsibility of Joint Auditors” deals with the professional responsibilities, which the

auditors undertake in accepting such appointments as joint auditors. In respect of the work divided

amongst the joint auditors, each joint auditor is responsible only for the work allocated to him,

www.auditguru.in PARAM 2.19 | P a g e