Page 7 - Chap3 Composition Levy

P. 7

turnover in preceding financial year is Nil.

Ü Consequently, it is eligible to avail the composition scheme u/s 10(2A) of CGST Act in current financial year.

Ü It becomes liable to the registration when its aggregate turnover exceeds ` 20 lakh. While registering under GST,

it has to opt for composition scheme under section 10(2A).

Ü Tax payable by the firm is as follows:

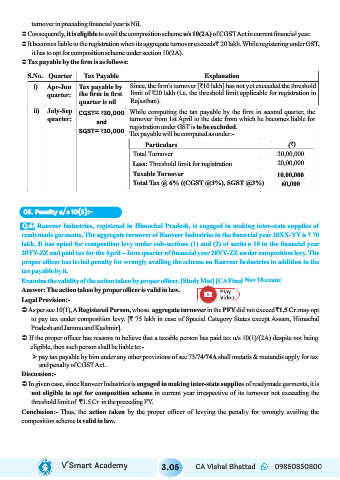

S.No. Quarter Tax Payable Explanation

i) Apr-Jun Tax payable by Since, the firm's turnover [₹10 lakh] has not yet exceeded the threshold

quarter: the firm in first limit of ₹20 lakh (i.e. the threshold limit applicable for registration in

quarter is nil Rajasthan).

ii) July-Sep CGST= `30,000 While computing the tax payable by the firm in second quarter, the

quarter: turnover from 1st April to the date from which he becomes liable for

and

registration under GST is to be excluded.

SGST= `30,000

Tax payable will be computed as under:-

Particulars (`)

Total Turnover 30,00,000

Less: Threshold limit for registration 20,00,000

Taxable Turnover 10,00,000

Total Tax @ 6% ((CGST @3%), SGST @3%) 60,000

03. Penalty u/s 10(5):-

Q.6: Ranveer Industries, registered in Himachal Pradesh, is engaged in making inter-state supplies of

readymade garments. The aggregate turnover of Ranveer Industries in the financial year 20XX-YY is ` 70

lakh. It has opted for composition levy under sub-sections (1) and (2) of section 10 in the financial year

20YY-ZZ and paid tax for the April – June quarter of financial year 20YY-ZZ under composition levy. The

proper officer has levied penalty for wrongly availing the scheme on Ranveer Industries in addition to the

tax payable by it.

Examine the validity of the action taken by proper officer. [Study Mat] [CA Final Nov 18 exam]

Answer: The action taken by proper officer is valid in law.

Legal Provision:-

Ü As per sec 10(1), A Registered Person, whose aggregate turnover in the PFY did not exceed `1.5 Cr.may opt

to pay tax under composition levy. [` 75 lakh in case of Special Category States except Assam, Himachal

Pradesh and Jammu and Kashmir].

Ü If the proper officer has reasons to believe that a taxable person has paid tax u/s 10(1)/(2A) despite not being

eligible, then such person shall be liable to:-

Ø pay tax payable by him under any other provisions of sec 73/74/74A shall mutatis & mutandis apply for tax

and penalty of CGST Act .

Discussion:-

Ü In given case, since Ranveer Industries is engaged in making inter-state supplies of readymade garments, it is

not eligible to opt for composition scheme in current year irrespective of its turnover not exceeding the

threshold limit of 1.5 Cr ` in the preceding FY.

Conclusion:- Thus, the action taken by the proper officer of levying the penalty for wrongly availing the

composition scheme is valid in law.

V’Smart Academy 3.05 CA Vishal Bhattad 09850850800