Page 9 - Chap3 Composition Levy

P. 9

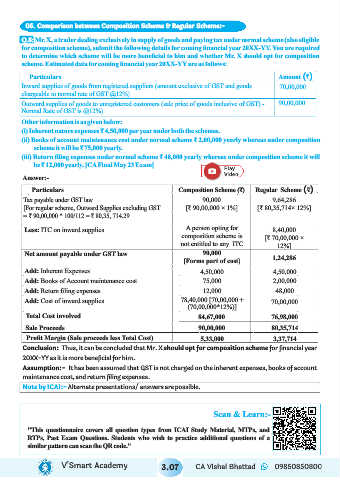

05. Comparison between Composition Scheme & Regular Scheme:-

Q.8: Mr. X, a trader dealing exclusively in supply of goods and paying tax under normal scheme (also eligible

for composition scheme), submit the following details for coming financial year 20XX-YY. You are required

to determine which scheme will be more beneficial to him and whether Mr. X should opt for composition

scheme. Estimated data for coming financial year 20XX-YY are as follows:

Particulars Amount (`)

Inward supplies of goods from registered suppliers (amount exclusive of GST and goods 70,00,000

chargeable to normal rate of GST @12%)

Outward supplies of goods to unregistered customers (sale price of goods inclusive of GST) - 90,00,000

Normal Rate of GST is @12%)

Other information is as given below:

(i) Inherent nature expenses ₹ 4,50,000 per year under both the schemes.

(ii) Books of account maintenance cost under normal scheme ₹ 2,00,000 yearly whereas under composition

scheme it will be ₹ 75,000 yearly.

(iii) Return filing expenses under normal scheme ₹ 48,000 yearly whereas under composition scheme it will

be ₹ 12,000 yearly. [CA Final May 23 Exam]

Answer:-

Particulars Composition Scheme (₹) Regular Scheme (₹)

Tax payable under GST law 90,000 9,64,286

[For regular scheme, Outward Supplies excluding GST [₹ 90,00,000 × 1%] [₹ 80,35,714× 12%]

= ₹ 90,00,000 * 100/112 = ₹ 80,35, 714.29

Less: ITC on inward supplies A person opting for 8,40,000

composition scheme is [₹ 70,00,000 ×

not entitled to any ITC 12%]

Net amount payable under GST law 90,000 1,24,286

[Forms part of cost]

Add: Inherent Expenses 4,50,000 4,50,000

Add: Books of Account maintenance cost 75,000 2,00,000

Add: Return filing expenses 12,000 48,000

Add: Cost of inward supplies 78,40,000 [70,00,000 + 70,00,000

(70,00,000*12%)]

Total Cost involved 84,67,000 76,98,000

Sale Proceeds 90,00,000 80,35,714

Profit Margin (Sale proceeds less Total Cost) 5,33,000 3,37,714

Conclusion: Thus, it can be concluded that Mr. X should opt for composition scheme for financial year

20XX-YY as it is more beneficial for him.

Assumption:- It has been assumed that GST is not charged on the inherent expenses, books of account

maintenance cost, and return filing expenses.

Note by ICAI:- Alternate presentations/ answers are possible.

Scan & Learn:-

"This questionnaire covers all question types from ICAI Study Material, MTPs, and

RTPs, Past Exam Questions. Students who wish to practice additional questions of a

similar pattern can scan the QR code."

V’Smart Academy 3.07 CA Vishal Bhattad 09850850800