Page 7 - Chapter 5 TOS

P. 7

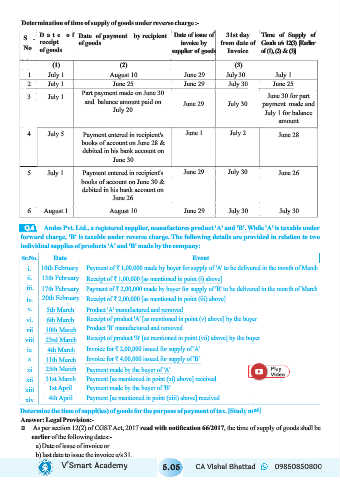

Determination of time of supply of goods under reverse charge :-

D a t e o f Date of payment by recipient Date of issue of 31st day Time of Supply of

S .

receipt of goods invoice by from date of Goods u/s 12(3) [Earlier

No of goods supplier of goods Invoice of (1), (2) & (3)]

(1) (2) (3)

1 July 1 August 10 June 29 July 30 July 1

2 July 1 June 25 June 29 July 30 June 25

Part payment made on June 30

3 July 1 June 30 for part

and balance amount paid on

June 29 July 30 payment made and

July 20

July 1 for balance

amount

4 July 5 Payment entered in recipient's June 1 July 2 June 28

books of account on June 28 &

debited in his bank account on

June 30

5 July 1 Payment entered in recipient's June 29 July 30 June 26

books of account on June 30 &

debited in his bank account on

June 26

6 August 1 August 10 June 29 July 30 July 30

Andes Pvt. Ltd., a registered supplier, manufactures product 'A' and 'B'. While 'A' is taxable under

Q.6

forward charge, 'B' is taxable under reverse charge. The following details are provided in relation to two

individual supplies of products 'A' and 'B' made by the company:

Sr.No. Date Event

i. 10th February Payment of ₹ 1,00,000 made by buyer for supply of 'A' to be delivered in the month of March

ii. 13th February Receipt of ₹ 1,00,000 [as mentioned in point (i) above]

iii. 17th February Payment of ₹ 2,00,000 made by buyer for supply of 'B' to be delivered in the month of March

iv. 20th February Receipt of ₹ 2,00,000 [as mentioned in point (iii) above]

v. 5th March Product 'A' manufactured and removed

vi. 6th March Receipt of product 'A' [as mentioned in point (v) above] by the buyer

vii 10th March Product 'B' manufactured and removed

viii 23rd March Receipt of product 'B' [as mentioned in point (vii) above] by the buyer

ix 4th March Invoice for ₹ 2,00,000 issued for supply of 'A’

x 11th March Invoice for ₹ 4,00,000 issued for supply of 'B’

xi 25th March Payment made by the buyer of 'A’

xii 31st March Payment [as mentioned in point (xi) above] received

xiii 1st April Payment made by the buyer of 'B’

xiv 4th April Payment [as mentioned in point (xiii) above] received

Determine the time of suppl(ies) of goods for the purpose of payment of tax. [Study mat]

Answer: Legal Provision:-

Ü As per section 12(2) of CGST Act, 2017 read with notification 66/2017, the time of supply of goods shall be

earlier of the following dates:-

a) Date of issue of invoice or

b) last date to issue the invoice u/s 31.

V’Smart Academy 5.05 CA Vishal Bhattad 09850850800