Page 9 - Chapter 5 TOS

P. 9

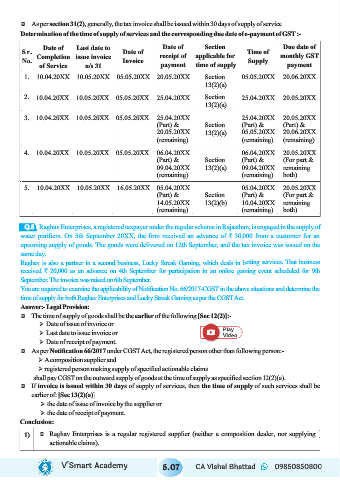

Ü As per section 31(2), generally, the tax invoice shall be issued within 30 days of supply of service

Determination of the time of supply of services and the corresponding due date of e-payment of GST :-

Date of Last date to Date of Section Due date of

S r. Date of Time of

Completion issue invoice receipt of applicable for monthly GST

No. Invoice Supply

of Service u/s 31 payment time of supply payment

1. 10.04.20XX 10.05.20XX 05.05.20XX 20.05.20XX Section 05.05.20XX 20.06.20XX

13(2)(a)

2. 10.04.20XX 10.05.20XX 05.05.20XX 25.04.20XX Section 25.04.20XX 20.05.20XX

13(2)(a)

3. 10.04.20XX 10.05.20XX 05.05.20XX 25.04.20XX 25.04.20XX 20.05.20XX

(Part) & Section (Part) & (Part) &

20.05.20XX 13(2)(a) 05.05.20XX 20.06.20XX

(remaining) (remaining) (remaining)

4. 10.04.20XX 10.05.20XX 05.05.20XX 06.04.20XX 06.04.20XX 20.05.20XX

(Part) & Section (Part) & (For part &

09.04.20XX 13(2)(a) 09.04.20XX remaining

(remaining) (remaining) both)

5. 10.04.20XX 10.05.20XX 16.05.20XX 05.04.20XX 05.04.20XX 20.05.20XX

(Part) & Section (Part) & (For part &

14.05.20XX 13(2)(b) 10.04.20XX remaining

(remaining) (remaining) both)

Q.8

Raghav Enterprises, a registered taxpayer under the regular scheme in Rajasthan, is engaged in the supply of

water purifiers. On 5th September 20XX, the firm received an advance of ₹ 30,000 from a customer for an

upcoming supply of goods. The goods were delivered on 12th September, and the tax invoice was issued on the

same day.

Raghav is also a partner in a second business, Lucky Streak Gaming, which deals in betting services. That business

received ₹ 20,000 as an advance on 4th September for participation in an online gaming event scheduled for 9th

September. The invoice was raised on 6th September.

You are required to examine the applicability of Notification No. 66/2017-CGST in the above situations and determine the

time of supply for both Raghav Enterprises and Lucky Streak Gaming as per the CGST Act.

Answer:- Legal Provision:

Ü The time of supply of goods shall be the earlier of the following [Sec 12(2)]:-

Ø Date of issue of invoice or

Ø Last date to issue invoice or

Ø Date of receipt of payment.

Ü As per Notification 66/2017 under CGST Act, the registered person other than following person:-

Ø A composition supplier and

Ø registered person making supply of specified actionable claims

shall pay CGST on the outward supply of goods at the time of supply as specified section 12(2)(a).

Ü If invoice is issued within 30 days of supply of services, then the time of supply of such services shall be

earlier of: [Sec 13(2)(a)]

Ø the date of issue of invoice by the supplier or

Ø the date of receipt of payment.

Conclusion:

1) Ü Raghav Enterprises is a regular registered supplier (neither a composition dealer, nor supplying

actionable claims).

V’Smart Academy 5.07 CA Vishal Bhattad 09850850800