Page 20 - Ch8_ EXEMPTION

P. 20

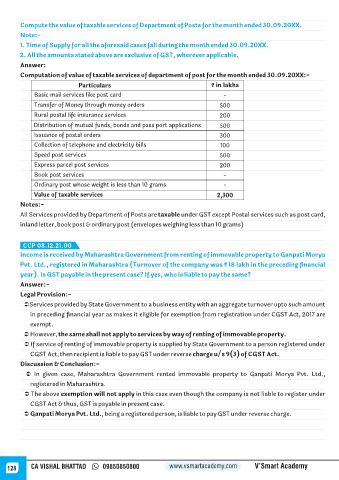

Compute the value of taxable services of Department of Posts for the month ended 30.09.20XX.

Note:-

1. Time of Supply for all the aforesaid cases fall during the month ended 30.09.20XX.

2. All the amounts stated above are exclusive of GST, wherever applicable.

Answer:

Computation of value of taxable services of department of post for the month ended 30.09.20XX:-

Particulars ₹ in lakhs

Basic mail services like post card -

Transfer of Money through money orders 500

Rural postal life insurance services 200

Distribution of mutual funds, bonds and pass port applications 500

Issuance of postal orders 300

Collection of telephone and electricity bills 100

Speed post services 500

Express parcel post services 200

Book post services -

Ordinary post whose weight is less than 10 grams -

Value of taxable services 2,300

Notes:-

All Services provided by Department of Posts are taxable under GST except Postal services such as post card,

inland letter, book post & ordinary post (envelopes weighing less than 10 grams)

CCP 08.12.21.00

Income is received by Maharashtra Government from renting of immovable property to Ganpati Morya

Pvt. Ltd., registered in Maharashtra (Turnover of the company was ₹ 18 lakh in the preceding financial

year). Is GST payable in the present case? If yes, who is liable to pay the same?

Answer:-

Legal Provision:-

ÜServices provided by State Government to a business entity with an aggregate turnover upto such amount

in preceding financial year as makes it eligible for exemption from registration under CGST Act, 2017 are

exempt.

Ü However, the same shall not apply to services by way of renting of immovable property.

Ü If service of renting of immovable property is supplied by State Government to a person registered under

CGST Act, then recipient is liable to pay GST under reverse charge u/s 9(3) of CGST Act.

Discussion & Conclusion:-

Ü In given case, Maharashtra Government rented immovable property to Ganpati Morya Pvt. Ltd.,

registered in Maharashtra.

Ü The above exemption will not apply in this case even though the company is not liable to register under

CGST Act & thus, GST is payable in present case.

Ü Ganpati Morya Pvt. Ltd., being a registered person, is liable to pay GST under reverse charge.

128 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy