Page 176 - CA Inter Audit PARAM

P. 176

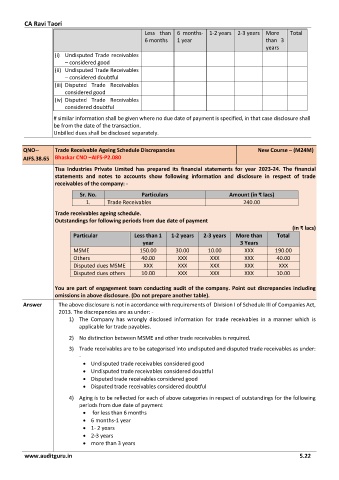

CA Ravi Taori

Less than 6 months- 1-2 years 2-3 years More Total

6 months 1 year than 3

years

(i) Undisputed Trade receivables

– considered good

(ii) Undisputed Trade Receivables

– considered doubtful

(iii) Disputed Trade Receivables

considered good

(iv) Disputed Trade Receivables

considered doubtful

# similar information shall be given where no due date of payment is specified, in that case disclosure shall

be from the date of the transaction.

Unbilled dues shall be disclosed separately.

QNO-- Trade Receivable Ageing Schedule Discrepancies New Course – (M24M)

AIFS.38.65 Bhaskar CNO –AIFS-P2.080

Tisa Industries Private Limited has prepared its financial statements for year 2023-24. The financial

statements and notes to accounts show following information and disclosure in respect of trade

receivables of the company: -

Sr. No. Particulars Amount (in ₹ lacs)

1. Trade Receivables 240.00

Trade receivables ageing schedule.

Outstandings for following periods from due date of payment

(in ₹ lacs)

Particular Less than 1 1-2 years 2-3 years More than Total

year 3 Years

MSME 150.00 30.00 10.00 XXX 190.00

Others 40.00 XXX XXX XXX 40.00

Disputed dues MSME XXX XXX XXX XXX XXX

Disputed dues others 10.00 XXX XXX XXX 10.00

You are part of engagement team conducting audit of the company. Point out discrepancies including

omissions in above disclosure. (Do not prepare another table).

Answer The above disclosure is not in accordance with requirements of Division I of Schedule III of Companies Act,

2013. The discrepancies are as under: -

1) The Company has wrongly disclosed information for trade receivables in a manner which is

applicable for trade payables.

2) No distinction between MSME and other trade receivables is required.

3) Trade receivables are to be categorised into undisputed and disputed trade receivables as under:

-

• Undisputed trade receivables considered good

• Undisputed trade receivables considered doubtful

• Disputed trade receivables considered good

• Disputed trade receivables considered doubtful

4) Aging is to be reflected for each of above categories in respect of outstandings for the following

periods from due date of payment

• for less than 6 months

• 6 months-1 year

• 1- 2 years

• 2-3 years

• more than 3 years

www.auditguru.in 5.22