Page 191 - CA Inter Audit PARAM

P. 191

CA Ravi Taori

QNO Disclosure related to CRPYPTO Currency (Virtual) Old Course -- (N22E)

AIFS.90 Bhaskar CNO - AIFS-P3.130

A Ltd. has traded for 50.00 Lacs in "TETRA", a virtual currency, during the F.Y. 2021-2022 and earned a profit

of 20.00 Lacs on it. What disclosure requirements are prescribed for such type of transactions done by the

company?

Answer Disclosure of Crypto Currency or Virtual Currency:

Where the Company has traded or invested in Crypto currency or Virtual Currency during the financial year,

the following shall be disclosed:

(a) profit or loss on transactions involving Crypto currency or Virtual Currency

(b) amount of currency held as at the reporting date,

(c) deposits or advances from any person for the purpose of trading or investing in Crypto Currency/

virtual currency.

QNO— Disclosure of Ratios New Course – (SM25/S24E)

AIFS.92 Bhaskar CNO - AIFS-P3.130

Various ratios of current year and preceding year are disclosed in financial statements of a company in

accordance with requirements of Schedule III of Companies Act, 2013. Discuss requirements of law in

this regard (Do not list out names of ratios)

Answer Following Ratios to be disclosed; -

• Current Ratio,

• Debt-Equity Ratio,

• Debt Service Coverage Ratio,

• Return on Equity Ratio,

• Inventory turnover ratio,

• Trade Receivables turnover ratio,

• Trade payables turnover ratio,

• Net capital turnover ratio,

• Net profit ratio,

• Return on Capital employed,

• Return on investment.

• The company shall explain the items included in numerator and denominator for computing the

above ratios. Further explanation shall be provided for any change in the ratio by more than 2S%

as compared to the preceding year.

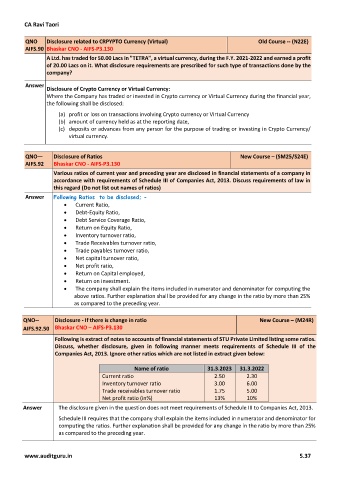

QNO-- Disclosure - If there is change in ratio New Course – (M24R)

AIFS.92.50 Bhaskar CNO – AIFS-P3.130

Following is extract of notes to accounts of financial statements of STU Private Limited listing some ratios.

Discuss, whether disclosure, given in following manner meets requirements of Schedule III of the

Companies Act, 2013. Ignore other ratios which are not listed in extract given below:

Name of ratio 31.3.2023 31.3.2022

Current ratio 2.50 2.30

Inventory turnover ratio 3.00 6.00

Trade receivables turnover ratio 1.75 5.00

Net profit ratio (in%) 13% 10%

Answer The disclosure given in the question does not meet requirements of Schedule III to Companies Act, 2013.

Schedule III requires that the company shall explain the items included in numerator and denominator for

computing the ratios. Further explanation shall be provided for any change in the ratio by more than 25%

as compared to the preceding year.

www.auditguru.in 5.37