Page 309 - CA Inter Audit PARAM

P. 309

CA Ravi Taori

• Vouching payment of grants, also verifying that the grants have been paid only for a

charitable purpose or purposes falling within the purview of the objects for which the

charitable institution has been set up and that no trustee, director or member of the

Managing Committee has benefited there from either directly or indirectly.

• Ascertaining that any funds contributed for a special purpose have been utilized for the purpose.

➢ Major Assets

• Verifying the schedules of securities held, as well as inventories of properties both movable and

immovable by inspecting the securities and title deeds of property and by physical verification of

the movable properties on a test- basis.

• Verifying the cash and bank balances.

➢ Other Points

• Income Tax Refunds – Where income-tax has been deducted from the Investment income, it should be

seen that a refund thereof has been obtained since charitable institutions are exempt from

payment of Income-tax. This involves:

• vouching the Income-tax refund with the correspondence with the Income- tax

Department; and

• checking the calculation of the repayment of claims.

Author’s Note

• This is a master answer you can write the relevant aspect of the master answer as per what

the question is asking.

• In study Material they have included points of assets also in audit of expenditure

Audit of an NGO Old Course –

QNO (Receipts & Remittances (P16M/N17R/N18E/N18R/M21M/SM17/M18M/N18M/M19M/SM20/SM21)

ADE.75

New Course – (SM25/J25R)

to Others) #Unique

An NGO operating in Delhi had collected large scale donations for Tsunami victims. The donations so

collected were sent to different NGOs operating in Tamil Nadu for relief operations. This NGO operating in

Delhi has appointed you to audit its accounts for the year in which it collected and remitted donations for

Tsunami victims. Draft audit programme for audit of receipts of donations and remittance of the collected

amount to different NGOs. Mention two points each, peculiar to the situation, which you will like to

incorporate in your audit programme for audit of said receipts and remittances of donations.

OR

"An NGO operating in Mumbai has collected large scale donations for Kerala flood victims. This NGO has

appointed you to audit its accounts for the specific period in which it collected donations. Draft audit

programme, mentioning six points peculiar to the situation, which you would like to incorporate in your

audit programme."

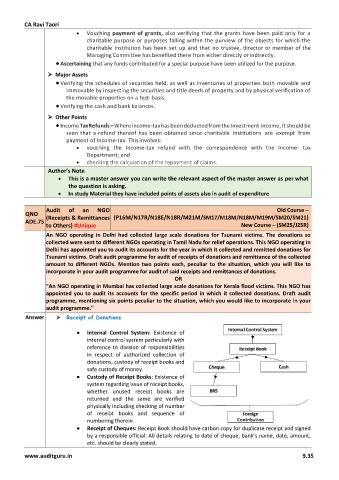

Answer ➢ Receipt of Donations

• Internal Control System: Existence of

internal control system particularly with

reference to division of responsibilities

in respect of authorized collection of

donations, custody of receipt books and

safe custody of money.

• Custody of Receipt Books: Existence of

system regarding issue of receipt books,

whether unused receipt books are

returned and the same are verified

physically including checking of number

of receipt books and sequence of

numbering therein.

• Receipt of Cheques: Receipt Book should have carbon copy for duplicate receipt and signed

by a responsible official. All details relating to date of cheque, bank’s name, date, amount,

etc. should be clearly stated.

www.auditguru.in 9.35