Page 32 - CA Inter Audit PARAM

P. 32

CA Ravi Taori

where withdrawal is permitted by law or regulation. The engagement partner shall promptly

report to the firm any inability to resolve the matter for appropriate action.

Authors Note -- Responsibility of Engagement Partner with respect to Independence is covered in SA 300

& SA 220 and both are same. Can give reference of Both and explain this fact.

Factors for establishing Overall Audit Old Course -- (M16R/M17R/M22M/N23R)

QNO

Strategy New Course(J25M)

300.03

Bhaskar CNO SA300.020

“In establishing the overall audit strategy, the auditor shall, among other considerations, ascertain the

nature, timing and extent of resources necessary to perform the engagement”. Explain those

considerations in detail.

OR

Explain the factors an auditor would consider in establishing the overall audit strategy.

OR

Discuss the factors the auditor will consider while establishing the overall strategy

Answer In establishing the overall audit strategy, the auditor shall:

(i) Identify the characteristics of the engagement that define its scope

(ii) Ascertain the reporting objectives of the engagement to plan the timing of the audit and

the nature of the communications required;

(iii) Consider the factors that, in the auditor’s professional judgment, are significant in directing

the engagement team’s efforts;

(iv) Consider the results of preliminary engagement activities and, where applicable, whether

knowledge gained on other engagements performed by the engagement partner for the

entity is relevant; and

(v) Ascertain the nature, timing and extent of resources necessary to perform the

engagement.

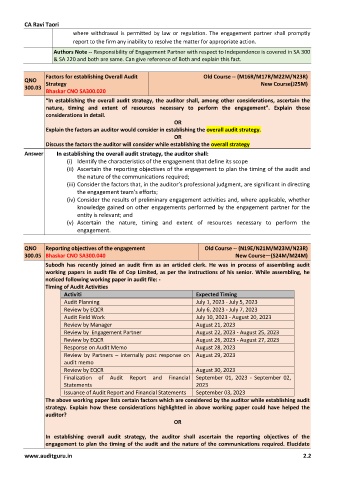

QNO Reporting objectives of the engagement Old Course -- (N19E/N21M/M23M/N23R)

300.05 Bhaskar CNO SA300.040 New Course—(S24M/M24M)

Subodh has recently joined an audit firm as an articled clerk. He was in process of assembling audit

working papers in audit file of Cop Limited, as per the instructions of his senior. While assembling, he

noticed following working paper in audit file: -

Timing of Audit Activities

Activiti Expected Timing

Audit Planning July 1, 2023 - July 5, 2023

Review by EQCR July 6, 2023 - July 7, 2023

Audit Field Work July 10, 2023 - August 20, 2023

Review by Manager August 21, 2023

Review by Engagement Partner August 22, 2023 - August 25, 2023

Review by EQCR August 26, 2023 - August 27, 2023

Response on Audit Memo August 28, 2023

Review by Partners – internally post response on August 29, 2023

audit memo

Review by EQCR August 30, 2023

Finalization of Audit Report and Financial September 01, 2023 - September 02,

Statements 2023

Issuance of Audit Report and Financial Statements September 03, 2023

The above working paper lists certain factors which are considered by the auditor while establishing audit

strategy. Explain how these considerations highlighted in above working paper could have helped the

auditor?

OR

In establishing overall audit strategy, the auditor shall ascertain the reporting objectives of the

engagement to plan the timing of the audit and the nature of the communications required. Elucidate

www.auditguru.in 2.2