Page 58 - CA Inter Audit PARAM

P. 58

CA Ravi Taori

procedures at the assertion level necessary to obtain sufficient appropriate audit evidence.

In identifying and assessing risks of material misstatement at the assertion level, the auditor may

conclude that the identified risks relate more pervasively to the financial statements as a whole

and potentially affect many assertions. Assertions used by the auditor to consider the different

types of potential misstatements that may occur fall into the following three categories and may

take the following forms –

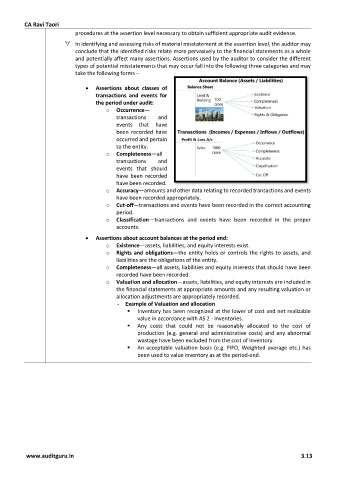

• Assertions about classes of

transactions and events for

the period under audit:

o Occurrence—

transactions and

events that have

been recorded have

occurred and pertain

to the entity.

o Completeness—all

transactions and

events that should

have been recorded

have been recorded.

o Accuracy—amounts and other data relating to recorded transactions and events

have been recorded appropriately.

o Cut-off—transactions and events have been recorded in the correct accounting

period.

o Classification—transactions and events have been recorded in the proper

accounts.

• Assertions about account balances at the period end:

o Existence—assets, liabilities, and equity interests exist.

o Rights and obligations—the entity holds or controls the rights to assets, and

liabilities are the obligations of the entity.

o Completeness—all assets, liabilities and equity interests that should have been

recorded have been recorded.

o Valuation and allocation—assets, liabilities, and equity interests are included in

the financial statements at appropriate amounts and any resulting valuation or

allocation adjustments are appropriately recorded.

- Example of Valuation and allocation

▪ Inventory has been recognized at the lower of cost and net realizable

value in accordance with AS 2 - Inventories.

▪ Any costs that could not be reasonably allocated to the cost of

production (e.g. general and administrative costs) and any abnormal

wastage have been excluded from the cost of inventory.

▪ An acceptable valuation basis (e.g. FIFO, Weighted average etc.) has

been used to value inventory as at the period-end.

www.auditguru.in 3.13