Page 87 - CA Inter Audit PARAM

P. 87

CA Ravi Taori

➢ The risks arising from the characteristics of the control, including whether it is Manual or

automated;

(Quotation Selection & Issuing PO is subjective matter and depends on approving

authority, behavior can change over period of time)

➢ The effectiveness of General IT-controls;

(Purchase entries are ID restricted, but people use each other’s computer, and they

know username passwords)

➢ The effectiveness of the control and its application by the entity, including the nature and extent

of deviations in the application of the control noted in previous audits, and whether there have

been Personnel changes that significantly affect the application of the control;

(Purchase & Store Manager Retired at the beginning of the year, they were replaced

my new comers)

➢ Whether the lack of a change in a particular control poses a risk due to Changing circumstances;

and (GST)

➢ The risks of Material misstatement and the extent of reliance on the control.

(Higher risk less reliance on previous year evidence)

Specific inquiries by auditor when deviations from Old Course - (M19R/ N20E/M21M/

QNO

330.13 controls are detected SM17/M18E/SM20/SM21)

Bhaskar CNO SA330.080

XYZ & Associates, Chartered Accountants, while evaluating the operating effectiveness of internal controls,

detects deviation from controls. In such a situation, state the specific inquiries to be made by an auditor to

understand these matters and their potential consequences.

OR

When deviations from controls upon which the auditor intends to rely are detected, the auditor shall make

specific inquiries to understand these matters and their potential consequences Explain.

Answer

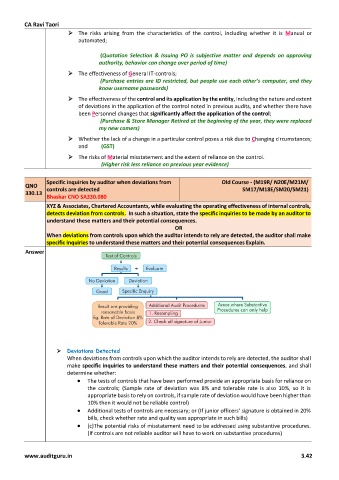

➢ Deviations Detected

When deviations from controls upon which the auditor intends to rely are detected, the auditor shall

make specific inquiries to understand these matters and their potential consequences, and shall

determine whether:

• The tests of controls that have been performed provide an appropriate basis for reliance on

the controls; (Sample rate of deviation was 8% and tolerable rate is also 10%, so it is

appropriate basis to rely on controls, if sample rate of deviation would have been higher than

10% then it would not be reliable control)

• Additional tests of controls are necessary; or (If junior officers’ signature is obtained in 20%

bills, check whether rate and quality was appropriate in such bills)

• (c)The potential risks of misstatement need to be addressed using substantive procedures.

(If controls are not reliable auditor will have to work on substantive procedures)

www.auditguru.in 3.42