Page 10 - Chapter 1

P. 10

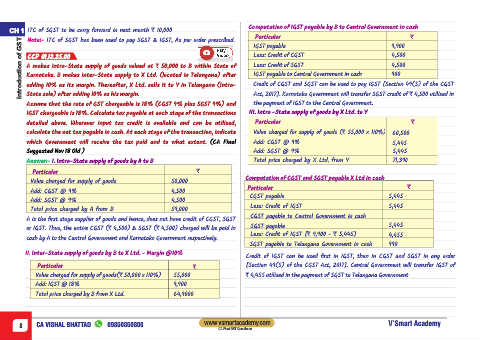

CH 1 ITC of SGST to be carry forward in next month ` 10,000 Computation of IGST payable by B to Central Government in cash

Particular 9,900 `

Note:-

ITC of SGST has been used to pay SGST & IGST, As per order prescribed.

Introduction of GST A makes intra-State supply of goods valued at ` 50,000 to B within State of Less: Credit of CGST 4,500

IGST payable

CCP 01.12.25.00

Less: Credit of SGST

4,500

IGST payable to Central Government in cash

900

Karnatake. B makes inter-State supply to X Ltd. (located in Telangana) after

Credit of CGST and SGST can be used to pay IGST [Section 49(5) of the CGST

adding 10% as its margin. Thereafter, X Ltd. sells it to Y in Telangana (Intra-

State sale) after adding 10% as his margin.

Assume that the rate of GST chargeable is 18% (CGST 9% plus SGST 9%) and Act, 2017]. Karnataka Government will transfer SGST credit of ` 4,500 utilised in

the payment of IGST to the Central Government.

IGST chargeable is 18%. Calculate tax payable at each stage of the transactions III. Intra -State supply of goods by X Ltd. to Y

detailed above. Wherever input tax credit is available and can be utilized, Particular `

calculate the net tax payable in cash. At each stage of the transaction, indicate Value charged for supply of goods (` 55,000 x 110%) 60,500

which Government will receive the tax paid and to what extent. (CA Final Add: CGST @ 9% 5,445

Suggested Nov 18 Old ) Add: SGST @ 9% 5,445

Answer:- I. Intra-State supply of goods by A to B Total price charged by X Ltd. from Y 71,390

Particular `

Computation of CGST and SGST payable X Ltd in cash

Value charged for supply of goods 50,000

Particular `

Add: CGST @ 9% 4,500

CGST payable 5,445

Add: SGST @ 9% 4,500

Less: Credit of IGST 5,445

Total price charged by A from B 59,000

CGST payable to Central Government in cash Nil

A is the first stage supplier of goods and hence, does not have credit of CGST, SGST

SGST payable 5,445

or IGST. Thus, the entire CGST (` 4,500) & SGST (` 4,500) charged will be paid in

Less: Credit of IGST [` 9,900 - ` 5,445] 4,455

cash by A to the Central Government and Karnataka Government respectively.

SGST payable to Telangana Government in cash 990

II. Inter-State supply of goods by B to X Ltd. - Margin @10%

Credit of IGST can be used first in IGST, then in CGST and SGST in any order

Particular ` [Section 49(5) of the CGST Act, 2017]. Central Government will transfer IGST of

Value charged for supply of goods(` 50,000 x 110%) 55,000 ` 4,455 utilised in the payment of SGST to Telangana Government

Add: IGST @ 18% 9,900

Total price charged by B from X Ltd. 64,9000

www.vsmartacademy.com

8 CA VISHAL BHATTAD 09850850800 V’Smart Academy

CA Final GST Questioner