Page 9 - Chapter 1

P. 9

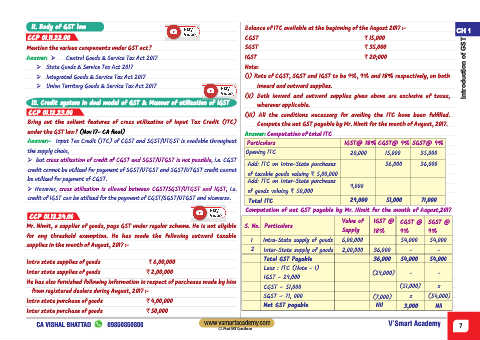

11. Body of GST law Balance of ITC available at the beginning of the August 2017 :-

CH 1

CCP 01.11.22.00 CGST ` 15,000

Mention the various components under GST act? SGST ` 35,000

Answer: Ø Central Goods & Service Tax Act 2017 IGST ` 20;000

Ø State Goods & Service Tax Act 2017 Note: Introduction of GST

Ø Integrated Goods & Service Tax Act 2017 (i) Rate of CGST, SGST and IGST to be 9%, 9% and 18% respectively, on both

Ø Union Territory Goods & Service Tax Act 2017 inward and outward supplies.

(ii) Both inward and outward supplies given above are exclusive of taxes,

12. Credit system in dual model of GST & Manner of utilization of IGST

wherever applicable.

CCP 01.12.23.00

(iii) All the conditions necessary for availing the ITC have been fulfilled.

Bring out the salient features of cross utilization of Input Tax Credit (ITC)

Compute the net GST payable by Mr. Nimit for the month of August, 2017.

under the GST law? (Nov 17- CA final)

Answer: Computation of total ITC

Answer:- Input Tax Credit (ITC) of CGST and SGST/UTGST is available throughout Particulars IGST@ 18% CGST@ 9% SGST@ 9%

the supply chain, Opening ITC 20,000 15,000 35,000

Ø but cross utilization of credit of CGST and SGST/UTGST is not possible , i.e. CGST

Add: ITC on Intra-State purchases 36,000 36,000

credit cannot be utilized for payment of SGST/UTGST and SGST/UTGST credit cannot

of taxable goods valuing ` 5,00,000

be utilized for payment of CGST. Add: ITC on Inter-State purchases

9,000

Ø However, cross utilization is allowed between CGST/SGST/UTGST and IGST, i.e.

of goods valuing ` 50,000

credit of IGST can be utilized for the payment of CGST/SGST/UTGST and viceversa.

Total ITC 29,000 51,000 71,000

Computation of net GST payable by Mr. Nimit for the month of August,2017

CCP 01.12.24.00

Value of IGST @ CGST @ SGST @

Mr. Nimit, a supplier of goods, pays GST under regular scheme. He is not eligible S. No. Particulars

Supply 18% 9% 9%

for any threshold exemption. He has made the following outward taxable

1 Intra-State supply of goods 6,00,000 54,000 54,000

supplies in the month of August, 2017 :-

2 Inter-State supply of goods 2,00,000 36,000 - -

Intra state supplies of goods ` 6,00,000 Total GST Payable 36,000 54,000 54,000

Less : ITC (Note - 1)

Inter state supplies of goods ` 2,00,000 (29,000) - -

IGST - 29,000

He has also furnished following information in respect of purchases made by him

CGST – 51,000 (51,000) x

from registered dealers during August, 2017 :-

SGST – 71, 000 (7,000) x (54,000)

Intra state purchase of goods ` 4,00,000

Net GST payable Nil 3,000 Nil

Inter state purchase of goods ` 50,000

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 7

CA Final GST Questioner