Page 13 - CHAPTER 3 (1).cdr

P. 13

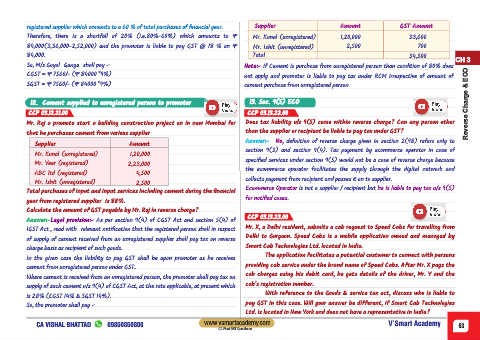

registered supplier which amounts to a 60 % of total purchases of financial year. Supplier Amount GST Amount

Therefore, there is a shortfall of 20% (i.e.80%-60%) which amounts to ₹ Mr. Kunal (unregistered) 1,20,000 33,600

84,000(3,36,000-2,52,000) and the promoter is liable to pay GST @ 18 % on ₹ Mr. Ishit (unregistered) 2,500 700

84,000. Total 34,300

CH 3

So, M/s Goyal Ganga shall pay –

Note:- If Cement is purchase from unregistered person than condition of 80% does

Reverse Charge & ECO

CGST = ₹ 7560/- (₹ 84000 *9%) not apply and promoter is liable to pay tax under RCM irrespective of amount of

SGST = ₹ 7560/- (₹ 84000 *9%)

cement purchase from unregistered person

12. Cement supplied to unregistered person to promotor 13. Sec. 9(5) ECO

CCP 03.12.21.00 CCP 03.13.22.00

Mr. Raj a promote start a building construction project on in new Mumbai for Does tax liability u/s 9(5) come within reverse charge? Can any person other

that he purchases cement from various supplier than the supplier or recipient be liable to pay tax under GST?

Supplier Amount Answer:- No, definition of reverse charge given in section 2(98) refers only to

section 9(3) and section 9(4). Tax payment by ecommerce operator in case of

Mr. Kunal (unregistered) 1,20,000

specified services under section 9(5) would not be a case of reverse charge because

Mr. Veer (registered) 2,23,000

the ecommerce operator facilitates the supply through the digital network and

ABC ltd (registered) 4,500

collects payment from recipient and passes it on to supplier.

Mr. Ishit (unregistered) 2,500

Ecommerce Operator is not a supplier / recipient but he is liable to pay tax u/s 9(5)

Total purchases of input and input services including cement during the financial

year from registered supplier is 88%. for notified cases.

Calculate the amount of GST payable by Mr. Raj in reverse charge?

CCP 03.13.23.00

Answer:-Legal provision:- As per section 9(4) of CGST Act and section 5(4) of

IGST Act , read with relevant notification that the registered person shall in respect Mr. X, a Delhi resident, submits a cab request to Speed Cabs for travelling from

of supply of cement received from an unregistered supplier shall pay tax on reverse Delhi to Gurgaon. Speed Cabs is a mobile application owned and managed by

charge basis as recipient of such goods. Smart Cab Technologies Ltd. located in India.

In the given case the liability to pay GST shall be upon promoter as he receives The application facilitates a potential customer to connect with persons

cement from unregistered person under GST. providing cab service under the brand name of Speed Cabs. After Mr. X pays the

Where cement is received from an unregistered person, the promoter shall pay tax on cab charges using his debit card, he gets details of the driver, Mr. Y and the

supply of such cement u/s 9(4) of CGST Act, at the rate applicable, at present which cab's registration number.

is 28% (CGST 14% & SGST 14%). With reference to the Goods & service tax act, discuss who is liable to

So, the promoter shall pay – pay GST in this case. Will your answer be different, if Smart Cab Technologies

Ltd. is located in New York and does not have a representative in India?

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 53

CA Final GST Questioner