Page 12 - 15. COMPILER QB - INDAS 21

P. 12

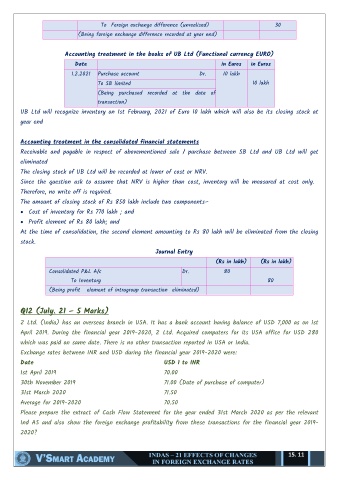

To Foreign exchange difference (unrealised) 30

(Being foreign exchange difference recorded at year end)

Accounting treatment in the books of UB Ltd (Functional currency EURO)

Date in Euros in Euros

1.2.2021 Purchase account Dr. 10 lakh

To SB limited 10 lakh

(Being purchased recorded at the date of

transaction)

UB Ltd will recognize inventory on 1st February, 2021 of Euro 10 lakh which will also be its closing stock at

year end

Accounting treatment in the consolidated financial statements

Receivable and payable in respect of abovementioned sale / purchase between SB Ltd and UB Ltd will get

eliminated

The closing stock of UB Ltd will be recorded at lower of cost or NRV.

Since the question ask to assume that NRV is higher than cost, inventory will be measured at cost only.

Therefore, no write off is required.

The amount of closing stock of Rs 850 lakh include two components–

Cost of inventory for Rs 770 lakh ; and

Profit element of Rs 80 lakh; and

At the time of consolidation, the second element amounting to Rs 80 lakh will be eliminated from the closing

stock.

Journal Entry

(Rs in lakh) (Rs in lakh)

Consolidated P&L A/c Dr. 80

To Inventory 80

(Being profit element of intragroup transaction eliminated)

Q12 (July. 21 – 5 Marks)

Z Ltd. (India) has an overseas branch in USA. It has a bank account having balance of USD 7,000 as on 1st

April 2019. During the financial year 2019-2020, Z Ltd. Acquired computers for its USA office for USD 280

which was paid on same date. There is no other transaction reported in USA or India.

Exchange rates between INR and USD during the financial year 2019-2020 were:

Date USD 1 to INR

1st April 2019 70.00

30th November 2019 71.00 (Date of purchase of computer)

31st March 2020 71.50

Average for 2019-2020 70.50

Please prepare the extract of Cash Flow Statement for the year ended 31st March 2020 as per the relevant

Ind AS and also show the foreign exchange profitability from these transactions for the financial year 2019-

2020?

15. 11