Page 4 - 16. COMPILER QB - INDAS 103

P. 4

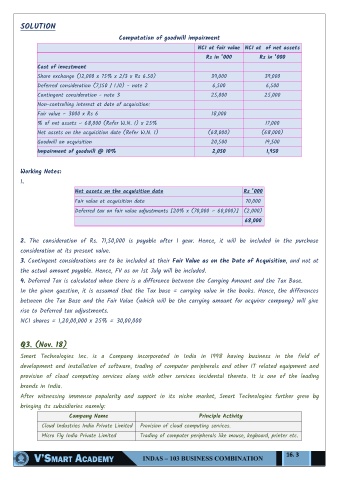

SOLUTION

Computation of goodwill impairment

NCI at fair value NCI at of net assets

Rs in ‘000 Rs in ‘000

Cost of investment

Share exchange (12,000 x 75% x 2/3 x Rs 6.50) 39,000 39,000

Deferred consideration (7,150 / 1.10) - note 2 6,500 6,500

Contingent consideration - note 3 25,000 25,000

Non-controlling interest at date of acquisition:

Fair value – 3000 x Rs 6 18,000

% of net assets – 68,000 (Refer W.N. 1) x 25% 17,000

Net assets on the acquisition date (Refer W.N. 1) (68,000) (68,000)

Goodwill on acquisition 20,500 19,500

Impairment of goodwill @ 10% 2,050 1,950

Working Notes:

1.

Net assets on the acquisition date Rs ’000

Fair value at acquisition date 70,000

Deferred tax on fair value adjustments [20% x (70,000 – 60,000)] (2,000)

68,000

2. The consideration of Rs. 71,50,000 is payable after 1 year. Hence, it will be included in the purchase

consideration at its present value.

3. Contingent considerations are to be included at their Fair Value as on the Date of Acquisition, and not at

the actual amount payable. Hence, FV as on 1st July will be included.

4. Deferred Tax is calculated when there is a difference between the Carrying Amount and the Tax Base.

In the given question, it is assumed that the Tax base = carrying value in the books. Hence, the differences

between the Tax Base and the Fair Value (which will be the carrying amount for acquirer company) will give

rise to Deferred tax adjustments.

NCI shares = 1,20,00,000 x 25% = 30,00,000

Q3. (Nov. 18)

Smart Technologies Inc. is a Company incorporated in India in 1998 having business in the field of

development and installation of software, trading of computer peripherals and other IT related equipment and

provision of cloud computing services along with other services incidental thereto. It is one of the leading

brands in India.

After witnessing immense popularity and support in its niche market, Smart Technologies further grew by

bringing its subsidiaries namely:

Company Name Principle Activity

Cloud Industries India Private Limited Provision of cloud computing services.

Micro Fly India Private Limited Trading of computer peripherals like mouse, keyboard, printer etc.

16. 3