Page 9 - 22. COMPILER QB - INDAS 34

P. 9

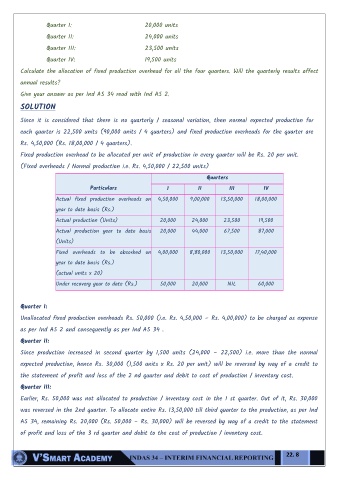

Quarter I: 20,000 units

Quarter II: 24,000 units

Quarter III: 23,500 units

Quarter IV: 19,500 units

Calculate the allocation of fixed production overhead for all the four quarters. Will the quarterly results affect

annual results?

Give your answer as per Ind AS 34 read with Ind AS 2.

SOLUTION

Since it is considered that there is no quarterly / seasonal variation, then normal expected production for

each quarter is 22,500 units (90,000 units / 4 quarters) and fixed production overheads for the quarter are

Rs. 4,50,000 (Rs. 18,00,000 / 4 quarters).

Fixed production overhead to be allocated per unit of production in every quarter will be Rs. 20 per unit.

(Fixed overheads / Normal production i.e. Rs. 4,50,000 / 22,500 units)

Quarters

Particulars I II III IV

Actual fixed production overheads on 4,50,000 9,00,000 13,50,000 18,00,000

year to date basis (Rs.)

Actual production (Units) 20,000 24,000 23,500 19,500

Actual production year to date basis 20,000 44,000 67,500 87,000

(Units)

Fixed overheads to be absorbed on 4,00,000 8,80,000 13,50,000 17,40,000

year to date basis (Rs.)

(actual units x 20)

Under recovery year to date (Rs.) 50,000 20,000 NIL 60,000

Quarter I:

Unallocated fixed production overheads Rs. 50,000 (i.e. Rs. 4,50,000 – Rs. 4,00,000) to be charged as expense

as per Ind AS 2 and consequently as per Ind AS 34 .

Quarter II:

Since production increased in second quarter by 1,500 units (24,000 – 22,500) i.e. more than the normal

expected production, hence Rs. 30,000 (1,500 units x Rs. 20 per unit) will be reversed by way of a credit to

the statement of profit and loss of the 2 nd quarter and debit to cost of production / inventory cost.

Quarter III:

Earlier, Rs. 50,000 was not allocated to production / inventory cost in the 1 st quarter. Out of it, Rs. 30,000

was reversed in the 2nd quarter. To allocate entire Rs. 13,50,000 till third quarter to the production, as per Ind

AS 34, remaining Rs. 20,000 (Rs. 50,000 – Rs. 30,000) will be reversed by way of a credit to the statement

of profit and loss of the 3 rd quarter and debit to the cost of production / inventory cost.

22. 8