Page 53 - 23. COMPILER QB - IND AS 109_32

P. 53

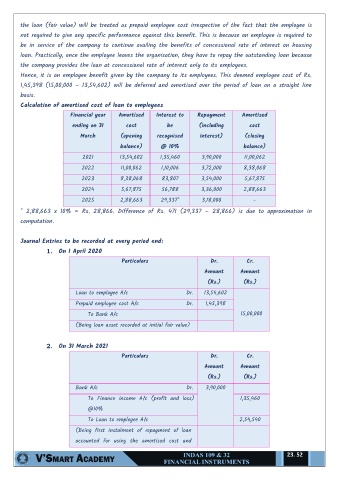

the loan (fair value) will be treated as prepaid employee cost irrespective of the fact that the employee is

not required to give any specific performance against this benefit. This is because an employee is required to

be in service of the company to continue availing the benefits of concessional rate of interest on housing

loan. Practically, once the employee leaves the organisation, they have to repay the outstanding loan because

the company provides the loan at concessional rate of interest only to its employees.

Hence, it is an employee benefit given by the company to its employees. This deemed employee cost of Rs.

1,45,398 (15,00,000 – 13,54,602) will be deferred and amortised over the period of loan on a straight line

basis.

Calculation of amortised cost of loan to employees

Financial year Amortised Interest to Repayment Amortised

ending on 31 cost be (including cost

March (opening recognised interest) (closing

balance) @ 10% balance)

2021 13,54,602 1,35,460 3,90,000 11,00,062

2022 11,00,062 1,10,006 3,72,000 8,38,068

2023 8,38,068 83,807 3,54,000 5,67,875

2024 5,67,875 56,788 3,36,000 2,88,663

2025 2,88,663 29,337* 3,18,000 -

* 2,88,663 x 10% = Rs. 28,866. Difference of Rs. 471 (29,337 – 28,866) is due to approximation in

computation.

Journal Entries to be recorded at every period end:

1. On 1 April 2020

Particulars Dr. Cr.

Amount Amount

(Rs.) (Rs.)

Loan to employee A/c Dr. 13,54,602

Prepaid employee cost A/c Dr. 1,45,398

To Bank A/c 15,00,000

(Being loan asset recorded at initial fair value)

2. On 31 March 2021

Particulars Dr. Cr.

Amount Amount

(Rs.) (Rs.)

Bank A/c Dr. 3,90,000

To Finance income A/c (profit and loss) 1,35,460

@10%

To Loan to employee A/c 2,54,540

(Being first instalment of repayment of loan

accounted for using the amortised cost and

23. 52