Page 55 - 23. COMPILER QB - IND AS 109_32

P. 55

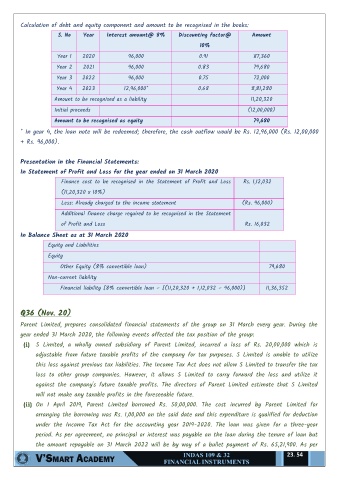

Calculation of debt and equity component and amount to be recognised in the books:

S. No Year Interest amount@ 8% Discounting factor@ Amount

10%

Year 1 2020 96,000 0.91 87,360

Year 2 2021 96,000 0.83 79,680

Year 3 2022 96,000 0.75 72,000

Year 4 2023 12,96,000* 0.68 8,81,280

Amount to be recognised as a liability 11,20,320

Initial proceeds (12,00,000)

Amount to be recognised as equity 79,680

* In year 4, the loan note will be redeemed; therefore, the cash outflow would be Rs. 12,96,000 (Rs. 12,00,000

+ Rs. 96,000).

Presentation in the Financial Statements:

In Statement of Profit and Loss for the year ended on 31 March 2020

Finance cost to be recognised in the Statement of Profit and Loss Rs. 1,12,032

(11,20,320 x 10%)

Less: Already charged to the income statement (Rs. 96,000)

Additional finance charge required to be recognised in the Statement

of Profit and Loss Rs. 16,032

In Balance Sheet as at 31 March 2020

Equity and Liabilities

Equity

Other Equity (8% convertible loan) 79,680

Non-current liability

Financial liability [8% convertible loan – [(11,20,320 + 1,12,032 – 96,000)] 11,36,352

Q36 (Nov. 20)

Parent Limited, prepares consolidated financial statements of the group on 31 March every year. During the

year ended 31 March 2020, the following events affected the tax position of the group:

(i) S Limited, a wholly owned subsidiary of Parent Limited, incurred a loss of Rs. 20,00,000 which is

adjustable from future taxable profits of the company for tax purposes. S Limited is unable to utilize

this loss against previous tax liabilities. The Income Tax Act does not allow S Limited to transfer the tax

loss to other group companies. However, it allows S Limited to carry forward the loss and utilize it

against the company's future taxable profits. The directors of Parent Limited estimate that S Limited

will not make any taxable profits in the foreseeable future.

(ii) On 1 April 2019, Parent Limited borrowed Rs. 50,00,000. The cost incurred by Parent Limited for

arranging the borrowing was Rs. 1,00,000 on the said date and this expenditure is qualified for deduction

under the Income Tax Act for the accounting year 2019-2020. The loan was given for a three-year

period. As per agreement, no principal or interest was payable on the loan during the tenure of loan but

the amount repayable on 31 March 2022 will be by way of a bullet payment of Rs. 65,21,900. As per

23. 54