Page 54 - 23. COMPILER QB - IND AS 109_32

P. 54

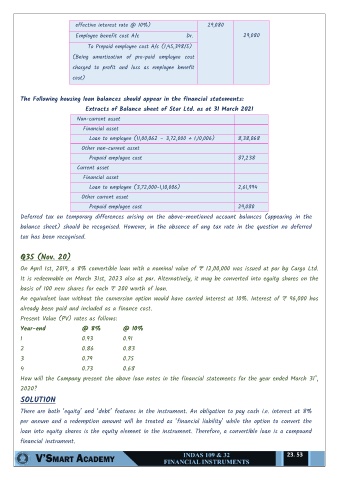

effective interest rate @ 10%) 29,080

Employee benefit cost A/c Dr. 29,080

To Prepaid employee cost A/c (1,45,398/5)

(Being amortization of pre-paid employee cost

charged to profit and loss as employee benefit

cost)

The Following housing loan balances should appear in the financial statements:

Extracts of Balance sheet of Star Ltd. as at 31 March 2021

Non-current asset

Financial asset

Loan to employee (11,00,062 – 3,72,000 + 1,10,006) 8,38,068

Other non-current asset

Prepaid employee cost 87,238

Current asset

Financial asset

Loan to employee (3,72,000-1,10,006) 2,61,994

Other current asset

Prepaid employee cost 29,080

Deferred tax on temporary differences arising on the above-mentioned account balances (appearing in the

balance sheet) should be recognised. However, in the absence of any tax rate in the question no deferred

tax has been recognised.

Q35 (Nov. 20)

On April 1st, 2019, a 8% convertible loan with a nominal value of ₹ 12,00,000 was issued at par by Cargo Ltd.

It is redeemable on March 31st, 2023 also at par. Alternatively, it may be converted into equity shares on the

basis of 100 new shares for each ₹ 200 worth of loan.

An equivalent loan without the conversion option would have carried interest at 10%. Interest of ₹ 96,000 has

already been paid and included as a finance cost.

Present Value (PV) rates as follows:

Year-end @ 8% @ 10%

1 0.93 0.91

2 0.86 0.83

3 0.79 0.75

4 0.73 0.68

How will the Company present the above loan notes in the financial statements for the year ended March 31",

2020?

SOLUTION

There are both ‘equity’ and ‘debt’ features in the instrument. An obligation to pay cash i.e. interest at 8%

per annum and a redemption amount will be treated as ‘financial liability’ while the option to convert the

loan into equity shares is the equity element in the instrument. Therefore, a convertible loan is a compound

financial instrument.

23. 53