Page 4 - 26. COMPILER QB - IND AS 113

P. 4

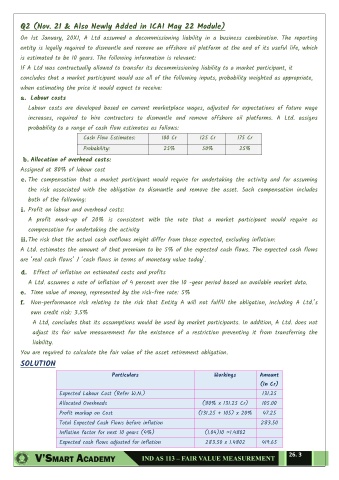

Q2 (Nov. 21 & Also Newly Added in ICAI May 22 Module)

On 1st January, 20X1, A Ltd assumed a decommissioning liability in a business combination. The reporting

entity is legally required to dismantle and remove an offshore oil platform at the end of its useful life, which

is estimated to be 10 years. The following information is relevant:

If A Ltd was contractually allowed to transfer its decommissioning liability to a market participant, it

concludes that a market participant would use all of the following inputs, probability weighted as appropriate,

when estimating the price it would expect to receive:

a. Labour costs

Labour costs are developed based on current marketplace wages, adjusted for expectations of future wage

increases, required to hire contractors to dismantle and remove offshore oil platforms. A Ltd. assigns

probability to a range of cash flow estimates as follows:

Cash Flow Estimates: 100 Cr 125 Cr 175 Cr

Probability: 25% 50% 25%

b. Allocation of overhead costs:

Assigned at 80% of labour cost

c. The compensation that a market participant would require for undertaking the activity and for assuming

the risk associated with the obligation to dismantle and remove the asset. Such compensation includes

both of the following:

i. Profit on labour and overhead costs:

A profit mark-up of 20% is consistent with the rate that a market participant would require as

compensation for undertaking the activity

ii. The risk that the actual cash outflows might differ from those expected, excluding inflation:

A Ltd. estimates the amount of that premium to be 5% of the expected cash flows. The expected cash flows

are ‘real cash flows’ / ‘cash flows in terms of monetary value today’.

d. Effect of inflation on estimated costs and profits

A Ltd. assumes a rate of inflation of 4 percent over the 10 -year period based on available market data.

e. Time value of money, represented by the risk-free rate: 5%

f. Non-performance risk relating to the risk that Entity A will not fulfill the obligation, including A Ltd.’s

own credit risk: 3.5%

A Ltd, concludes that its assumptions would be used by market participants. In addition, A Ltd. does not

adjust its fair value measurement for the existence of a restriction preventing it from transferring the

liability.

You are required to calculate the fair value of the asset retirement obligation.

SOLUTION

Particulars Workings Amount

(In Cr)

Expected Labour Cost (Refer W.N.) 131.25

Allocated Overheads (80% x 131.25 Cr) 105.00

Profit markup on Cost (131.25 + 105) x 20% 47.25

Total Expected Cash Flows before inflation 283.50

Inflation factor for next 10 years (4%) (1.04)10 =1.4802

Expected cash flows adjusted for inflation 283.50 x 1.4802 419.65

26. 3