Page 17 - 34.2 FR MARCH 22 MTP ANSWER

P. 17

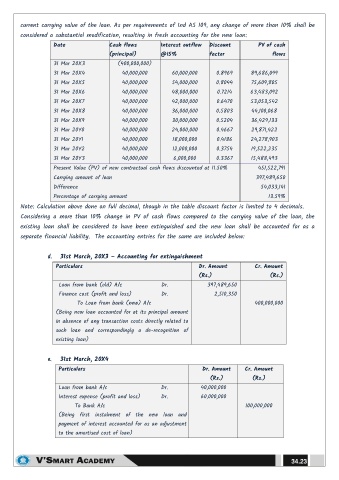

current carrying value of the loan. As per requirements of Ind AS 109, any change of more than 10% shall be

considered a substantial modification, resulting in fresh accounting for the new loan:

Date Cash flows Interest outflow Discount PV of cash

(principal) @15% factor flows

31 Mar 20X3 (400,000,000)

31 Mar 20X4 40,000,000 60,000,000 0.8969 89,686,099

31 Mar 20X5 40,000,000 54,000,000 0.8044 75,609,805

31 Mar 20X6 40,000,000 48,000,000 0.7214 63,483,092

31 Mar 20X7 40,000,000 42,000,000 0.6470 53,053,542

31 Mar 20X8 40,000,000 36,000,000 0.5803 44,100,068

31 Mar 20X9 40,000,000 30,000,000 0.5204 36,429,133

31 Mar 20Y0 40,000,000 24,000,000 0.4667 29,871,422

31 Mar 20Y1 40,000,000 18,000,000 0.4186 24,278,903

31 Mar 20Y2 40,000,000 12,000,000 0.3754 19,522,235

31 Mar 20Y3 40,000,000 6,000,000 0.3367 15,488,493

Present Value (PV) of new contractual cash flows discounted at 11.50% 451,522,791

Carrying amount of loan 397,489,650

Difference 54,033,141

Percentage of carrying amount 13.59%

Note: Calculation above done on full decimal, though in the table discount factor is limited to 4 decimals.

Considering a more than 10% change in PV of cash flows compared to the carrying value of the loan, the

existing loan shall be considered to have been extinguished and the new loan shall be accounted for as a

separate financial liability. The accounting entries for the same are included below:

d. 31st March, 20X3 – Accounting for extinguishment

Particulars Dr. Amount Cr. Amount

(Rs.) (Rs.)

Loan from bank (old) A/c Dr. 397,489,650

Finance cost (profit and loss) Dr. 2,510,350

To Loan from bank (new) A/c 400,000,000

(Being new loan accounted for at its principal amount

in absence of any transaction costs directly related to

such loan and correspondingly a de-recognition of

existing loan)

e. 31st March, 20X4

Particulars Dr. Amount Cr. Amount

(Rs.) (Rs.)

Loan from bank A/c Dr. 40,000,000

Interest expense (profit and loss) Dr. 60,000,000

To Bank A/c 100,000,000

(Being first instalment of the new loan and

payment of interest accounted for as an adjustment

to the amortised cost of loan)

34.23