Page 16 - 34.2 FR MARCH 22 MTP ANSWER

P. 16

release.

Solution 6

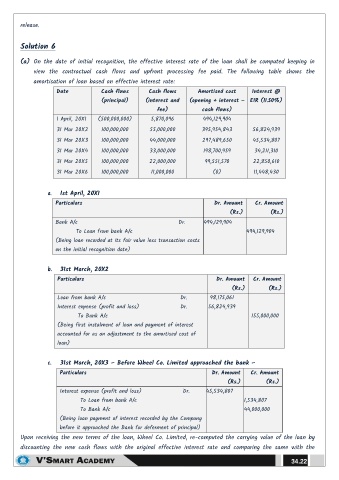

(a) On the date of initial recognition, the effective interest rate of the loan shall be computed keeping in

view the contractual cash flows and upfront processing fee paid. The following table shows the

amortisation of loan based on effective interest rate:

Date Cash flows Cash flows Amortised cost Interest @

(principal) (interest and (opening + interest – EIR (11.50%)

fee) cash flows)

1 April, 20X1 (500,000,000) 5,870,096 494,129,904

31 Mar 20X2 100,000,000 55,000,000 395,954,843 56,824,939

31 Mar 20X3 100,000,000 44,000,000 297,489,650 45,534,807

31 Mar 20X4 100,000,000 33,000,000 198,700,959 34,211,310

31 Mar 20X5 100,000,000 22,000,000 99,551,570 22,850,610

31 Mar 20X6 100,000,000 11,000,000 (0) 11,448,430

a. 1st April, 20X1

Particulars Dr. Amount Cr. Amount

(Rs.) (Rs.)

Bank A/c Dr. 494,129,904

To Loan from bank A/c 494,129,904

(Being loan recorded at its fair value less transaction costs

on the initial recognition date)

b. 31st March, 20X2

Particulars Dr. Amount Cr. Amount

(Rs.) (Rs.)

Loan from bank A/c Dr. 98,175,061

Interest expense (profit and loss) Dr. 56,824,939

To Bank A/c 155,000,000

(Being first instalment of loan and payment of interest

accounted for as an adjustment to the amortised cost of

loan)

c. 31st March, 20X3 – Before Wheel Co. Limited approached the bank –

Particulars Dr. Amount Cr. Amount

(Rs.) (Rs.)

Interest expense (profit and loss) Dr. 45,534,807

To Loan from bank A/c 1,534,807

To Bank A/c 44,000,000

(Being loan payment of interest recorded by the Company

before it approached the Bank for deferment of principal)

Upon receiving the new terms of the loan, Wheel Co. Limited, re-computed the carrying value of the loan by

discounting the new cash flows with the original effective interest rate and comparing the same with the

34.22