Page 14 - 34.2 FR MARCH 22 MTP ANSWER

P. 14

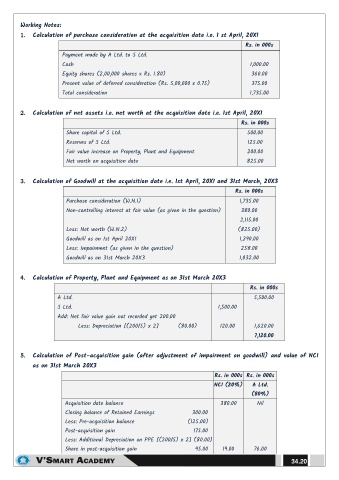

Working Notes:

1. Calculation of purchase consideration at the acquisition date i.e. 1 st April, 20X1

Rs. in 000s

Payment made by A Ltd. to S Ltd.

Cash 1,000.00

Equity shares (2,00,000 shares x Rs. 1.80) 360.00

Present value of deferred consideration (Rs. 5,00,000 x 0.75) 375.00

Total consideration 1,735.00

2. Calculation of net assets i.e. net worth at the acquisition date i.e. 1st April, 20X1

Rs. in 000s

Share capital of S Ltd. 500.00

Reserves of S Ltd. 125.00

Fair value increase on Property, Plant and Equipment 200.00

Net worth on acquisition date 825.00

3. Calculation of Goodwill at the acquisition date i.e. 1st April, 20X1 and 31st March, 20X3

Rs. in 000s

Purchase consideration (W.N.1) 1,735.00

Non-controlling interest at fair value (as given in the question) 380.00

2,115.00

Less: Net worth (W.N.2) (825.00)

Goodwill as on 1st April 20X1 1,290.00

Less: Impairment (as given in the question) 258.00

Goodwill as on 31st March 20X3 1,032.00

4. Calculation of Property, Plant and Equipment as on 31st March 20X3

Rs. in 000s

A Ltd. 5,500.00

S Ltd. 1,500.00

Add: Net fair value gain not recorded yet 200.00

Less: Depreciation [(200/5) x 2] (80.00) 120.00 1,620.00

7,120.00

5. Calculation of Post-acquisition gain (after adjustment of impairment on goodwill) and value of NCI

as on 31st March 20X3

Rs. in 000s Rs. in 000s

NCI (20%) A Ltd.

(80%)

Acquisition date balance 380.00 Nil

Closing balance of Retained Earnings 300.00

Less: Pre-acquisition balance (125.00)

Post-acquisition gain 175.00

Less: Additional Depreciation on PPE [(200/5) x 2] (80.00)

Share in post-acquisition gain 95.00 19.00 76.00

34.20