Page 2 - 35. FR APRIL 22 MTP QP ANSWERS

P. 2

MOCK TEST PAPER 2

FINAL COURSE: GROUP – I

PAPER – 1: FINANCIAL REPORTING

Question 1

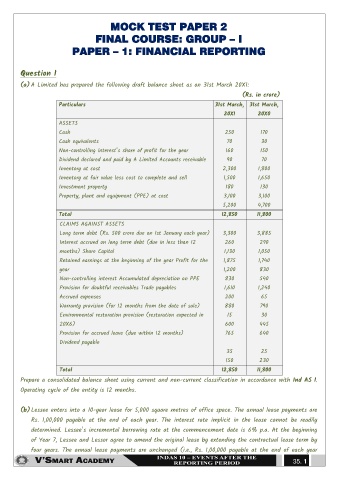

(a) A Limited has prepared the following draft balance sheet as on 31st March 20X1:

(Rs. in crore)

Particulars 31st March, 31st March,

20X1 20X0

ASSETS

Cash 250 170

Cash equivalents 70 30

Non-controlling interest’s share of profit for the year 160 150

Dividend declared and paid by A Limited Accounts receivable 90 70

Inventory at cost 2,300 1,800

Inventory at fair value less cost to complete and sell 1,500 1,650

Investment property 180 130

Property, plant and equipment (PPE) at cost 3,100 3,100

5,200 4,700

Total 12,850 11,800

CLAIMS AGAINST ASSETS

Long term debt (Rs. 500 crore due on 1st January each year) 3,300 3,885

Interest accrued on long term debt (due in less than 12 260 290

months) Share Capital 1,130 1,050

Retained earnings at the beginning of the year Profit for the 1,875 1,740

year 1,200 830

Non-controlling interest Accumulated depreciation on PPE 830 540

Provision for doubtful receivables Trade payables 1,610 1,240

Accrued expenses 200 65

Warranty provision (for 12 months from the date of sale) 880 790

Environmental restoration provision (restoration expected in 15 30

20X6) 600 445

Provision for accrued leave (due within 12 months) 765 640

Dividend payable

35 25

150 230

Total 12,850 11,800

Prepare a consolidated balance sheet using current and non-current classification in accordance with Ind AS 1.

Operating cycle of the entity is 12 months.

(b) Lessee enters into a 10-year lease for 5,000 square metres of office space. The annual lease payments are

Rs. 1,00,000 payable at the end of each year. The interest rate implicit in the lease cannot be readily

determined. Lessee’s incremental borrowing rate at the commencement date is 6% p.a. At the beginning

of Year 7, Lessee and Lessor agree to amend the original lease by extending the contractual lease term by

four years. The annual lease payments are unchanged (i.e., Rs. 1,00,000 payable at the end of each year

35. 1