Page 5 - Chapter 9 Registration

P. 5

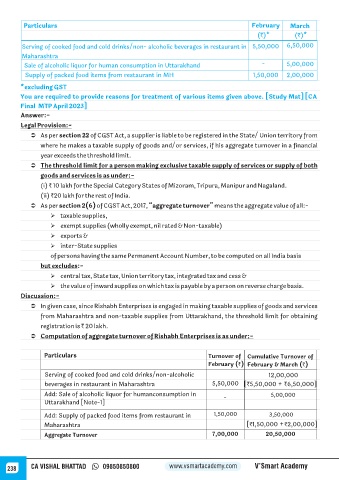

Particulars February March

(`)* (`)*

Serving of cooked food and cold drinks/non- alcoholic beverages in restaurant in 5,50,000 6,50,000

Maharashtra

Sale of alcoholic liquor for human consumption in Uttarakhand - 5,00,000

Supply of packed food items from restaurant in MH 1,50,000 2,00,000

*excluding GST

You are required to provide reasons for treatment of various items given above. [Study Mat] [CA

Final MTP April 2023]

Answer:-

Legal Provision:-

Ü As per section 22 of CGST Act, a supplier is liable to be registered in the State/ Union territory from

where he makes a taxable supply of goods and/or services, if his aggregate turnover in a financial

year exceeds the threshold limit.

Ü The threshold limit for a person making exclusive taxable supply of services or supply of both

goods and services is as under:-

(i) ` 10 lakh for the Special Category States of Mizoram, Tripura, Manipur and Nagaland.

(ii) `20 lakh for the rest of India.

Ü As per section 2(6) of CGST Act, 2017, “aggregate turnover” means the aggregate value of all:-

Ø taxable supplies,

Ø exempt supplies (wholly exempt, nil rated & Non-taxable)

Ø exports &

Ø inter-State supplies

of persons having the same Permanent Account Number, to be computed on all India basis

but excludes:-

Ø central tax, State tax, Union territory tax, integrated tax and cess &

Ø the value of inward supplies on which tax is payable by a person on reverse charge basis.

Discussion:-

Ü In given case, since Rishabh Enterprises is engaged in making taxable supplies of goods and services

from Maharashtra and non-taxable supplies from Uttarakhand, the threshold limit for obtaining

registration is ` 20 lakh.

Ü Computation of aggregate turnover of Rishabh Enterprises is as under:-

Particulars Turnover of Cumulative Turnover of

February (`) February & March (`)

Serving of cooked food and cold drinks/non-alcoholic 12,00,000

beverages in restaurant in Maharashtra 5,50,000 [`5,50,000 + `6,50,000]

Add: Sale of alcoholic liquor for humanconsumption in 5,00,000

-

Uttarakhand [Note-1]

Add: Supply of packed food items from restaurant in 1,50,000 3,50,000

Maharashtra [`1,50,000 +`2,00,000]

Aggregate Turnover 7,00,000 20,50,000

238 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy