Page 10 - Chapter 9 Registration

P. 10

05. Combined Questions on Section 22, 23 and 24:-

CCP 09.05.11.00

With the help of the following information in the case of M/s Jayant Enterprises, Jaipur (Rajasthan)

for the year 20XX-YY, determine the aggregate turnover for the purpose of registration under the

CGST Act, 2017.

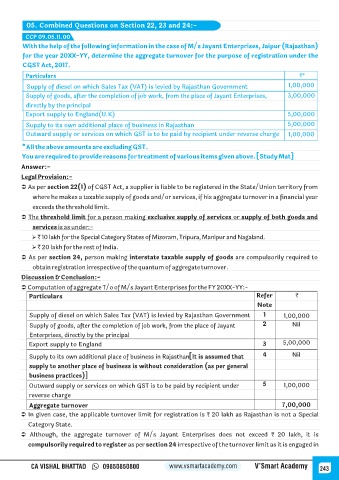

Particulars `*

Supply of diesel on which Sales Tax (VAT) is levied by Rajasthan Government 1,00,000

Supply of goods, after the completion of job work, from the place of Jayant Enterprises, 3,00,000

directly by the principal

Export supply to England(U.K) 5,00,000

Supply to its own additional place of business in Rajasthan 5,00,000

Outward supply or services on which GST is to be paid by recipient under reverse charge 1,00,000

*All the above amounts are excluding GST.

You are required to provide reasons for treatment of various items given above. [Study Mat]

Answer:-

Legal Provision:-

Ü As per section 22(1) of CGST Act, a supplier is liable to be registered in the State/Union territory from

where he makes a taxable supply of goods and/or services, if his aggregate turnover in a financial year

exceeds the threshold limit.

Ü The threshold limit for a person making exclusive supply of services or supply of both goods and

services is as under:-

Ø ` 10 lakh for the Special Category States of Mizoram, Tripura, Manipur and Nagaland.

Ø ` 20 lakh for the rest of India.

Ü As per section 24, person making interstate taxable supply of goods are compulsorily required to

obtain registration irrespective of the quantum of aggregate turnover.

Discussion & Conclusion:-

Ü Computation of aggregate T/o of M/s Jayant Enterprises for the FY 20XX-YY:-

Particulars Refer `

Note

Supply of diesel on which Sales Tax (VAT) is levied by Rajasthan Government 1 1,00,000

Supply of goods, after the completion of job work, from the place of Jayant 2 Nil

Enterprises, directly by the principal

Export supply to England 3 5,00,000

Supply to its own additional place of business in Rajasthan[It is assumed that 4 Nil

supply to another place of business is without consideration (as per general

business practices)]

Outward supply or services on which GST is to be paid by recipient under 5 1,00,000

reverse charge

Aggregate turnover 7,00,000

Ü In given case, the applicable turnover limit for registration is ₹ 20 lakh as Rajasthan is not a Special

Category State.

Ü Although, the aggregate turnover of M/s Jayant Enterprises does not exceed ₹ 20 lakh, it is

compulsorily required to register as per section 24 irrespective of the turnover limit as it is engaged in

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 243