Page 21 - Chap24Computation of GST

P. 21

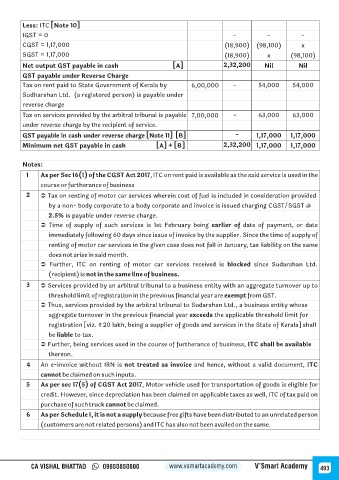

Less: ITC [Note 10]

IGST = 0 - - -

CGST = 1,17,000 (18,900) (98,100) x

SGST = 1,17,000 (18,900) x (98,100)

Net output GST payable in cash [A] 2,32,200 Nil Nil

GST payable under Reverse Charge

Tax on rent paid to State Government of Kerala by 6,00,000 - 54,000 54,000

Sudharshan Ltd. (a registered person) is payable under

reverse charge

Tax on services provided by the arbitral tribunal is payable 7,00,000 - 63,000 63,000

under reverse charge by the recipient of service.

GST payable in cash under reverse charge [Note 11] [B] - 1,17,000 1,17,000

Minimum net GST payable in cash [A] + [B] 2,32,200 1,17,000 1,17,000

Notes:

1 As per Sec 16(1) of the CGST Act 2017, ITC on rent paid is available as the said service is used in the

course or furtherance of business

2 Ü Tax on renting of motor car services wherein cost of fuel is included in consideration provided

by a non- body corporate to a body corporate and invoice is issued charging CGST/SGST @

2.5% is payable under reverse charge.

Ü Time of supply of such services is 1st February being earlier of date of payment, or date

immediately following 60 days since issue of invoice by the supplier. Since the time of supply of

renting of motor car services in the given case does not fall in January, tax liability on the same

does not arise in said month.

Ü Further, ITC on renting of motor car services received is blocked since Sudarshan Ltd.

(recipient) is not in the same line of business.

3 Ü Services provided by an arbitral tribunal to a business entity with an aggregate turnover up to

threshold limit of registration in the previous financial year are exempt from GST.

Ü Thus, services provided by the arbitral tribunal to Sudarshan Ltd., a business entity whose

aggregate turnover in the previous financial year exceeds the applicable threshold limit for

registration [viz. ₹ 20 lakh, being a supplier of goods and services in the State of Kerala] shall

be liable to tax.

Ü Further, being services used in the course of furtherance of business, ITC shall be available

thereon.

4 An e-invoice without IRN is not treated as invoice and hence, without a valid document, ITC

cannot be claimed on such inputs.

5 As per sec 17(5) of CGST Act 2017, Motor vehicle used for transportation of goods is eligible for

credit. However, since depreciation has been claimed on applicable taxes as well, ITC of tax paid on

purchase of such truck cannot be claimed.

6 As per Schedule I, it is not a supply because free gifts have been distributed to an unrelated person

(customers are not related persons) and ITC has also not been availed on the same.

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 493