Page 24 - Chap24Computation of GST

P. 24

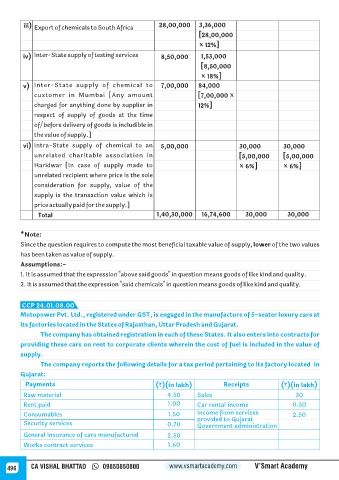

iii) Export of chemicals to South Africa 28,00,000 3,36,000

[28,00,000

× 12%]

iv) Inter-State supply of testing services 8,50,000 1,53,000

[8,50,000

× 18%]

v) Inter-State supply of chemical to 7,00,000 84,000

customer in Mumbai [Any amount [7,00,000 ×

charged for anything done by supplier in 12%]

respect of supply of goods at the time

of/before delivery of goods is includible in

the value of supply.]

vi) Intra-State supply of chemical to an 5,00,000 30,000 30,000

unrelated charitable association in [5,00,000 [5,00,000

Haridwar [In case of supply made to × 6%] × 6%]

unrelated recipient where price is the sole

consideration for supply, value of the

supply is the transaction value which is

price actually paid for the supply.]

Total 1,40,30,000 16,74,600 30,000 30,000

*Note:

Since the question requires to compute the most beneficial taxable value of supply, lower of the two values

has been taken as value of supply.

Assumptions:-

1. It is assumed that the expression "above said goods" in question means goods of like kind and quality.

2. It is assumed that the expression "said chemicals" in question means goods of like kind and quality.

CCP 24.01.08.00

Motopower Pvt. Ltd., registered under GST, is engaged in the manufacture of 5-seater luxury cars at

its factories located in the States of Rajasthan, Uttar Pradesh and Gujarat.

The company has obtained registration in each of these States. It also enters into contracts for

providing these cars on rent to corporate clients wherein the cost of fuel is included in the value of

supply.

The company reports the following details for a tax period pertaining to its factory located in

Gujarat:

Payments (`)(in lakh) Receipts (`)(in lakh)

Raw material 4.50 Sales 30

Rent paid 1.00 Car rental income 0.50

Consumables 1.50 Income from services 2.50

provided to Gujarat

Security services 0.70 Government administration

General insurance of cars manufactured 2.50

Works contract services 1.60

496 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy