Page 23 - Chap24Computation of GST

P. 23

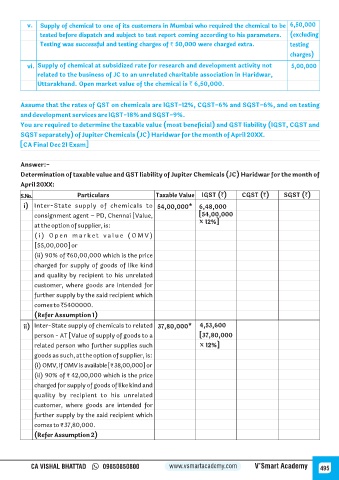

v. Supply of chemical to one of its customers in Mumbai who required the chemical to be 6,50,000

tested before dispatch and subject to test report coming according to his parameters. (excluding

Testing was successful and testing charges of ` 50,000 were charged extra. testing

charges)

vi. Supply of chemical at subsidized rate for research and development activity not 5,00,000

related to the business of JC to an unrelated charitable association in Haridwar,

Uttarakhand. Open market value of the chemical is ` 6,50,000.

Assume that the rates of GST on chemicals are lGST-12%, CGST-6% and SGST-6%, and on testing

and development services are lGST-18% and SGST-9%.

You are required to determine the taxable value (most beneficial) and GST liability (lGST, CGST and

SGST separately) of Jupiter Chemicals (JC) Haridwar for the month of April 20XX.

[CA Final Dec 21 Exam]

Answer:-

Determination of taxable value and GST liability of Jupiter Chemicals (JC) Haridwar for the month of

April 20XX:

S.No. Particulars Taxable Value IGST (`) CGST (`) SGST (`)

i) Inter-State supply of chemicals to 54,00,000* 6,48,000

consignment agent – PD, Chennai [Value, [54,00,000

× 12%]

at the option of supplier, is:

( i ) O p e n m a r k e t v a l u e ( O M V )

[55,00,000] or

(ii) 90% of `60,00,000 which is the price

charged for supply of goods of like kind

and quality by recipient to his unrelated

customer, where goods are intended for

further supply by the said recipient which

comes to `5400000.

(Refer Assumption 1)

ii) Inter-State supply of chemicals to related 37,80,000* 4,53,600

person - AT [Value of supply of goods to a [37,80,000

related person who further supplies such × 12%]

goods as such, at the option of supplier, is:

(i) OMV, if OMV is available [ 38,00,000] or₹

(ii) 90% of 42,00,000 which is the price ₹

charged for supply of goods of like kind and

quality by recipient to his unrelated

customer, where goods are intended for

further supply by the said recipient which

comes to 37,80,000. ₹

(Refer Assumption 2)

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 495