Page 22 - Chapter 6_Value of Supply

P. 22

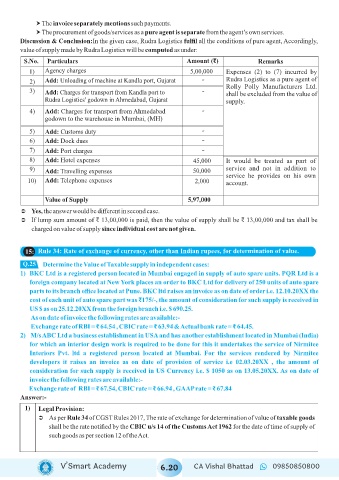

† The invoice separately mentions such payments.

† The procurement of goods/services as a pure agent is separate from the agent’s own services.

Discussion & Conclusion:In the given case, Rudra Logistics fulfil all the conditions of pure agent, Accordingly,

value of supply made by Rudra Logistics will be computed as under:

S.No. Particulars Amount ( )₹ Remarks

1) Agency charges 5,00,000 Expenses (2) to (7) incurred by

2) Add: Unloading of machine at Kandla port, Gujarat - Rudra Logistics as a pure agent of

Rolly Polly Manufacturers Ltd.

3) Add: Charges for transport from Kandla port to - shall be excluded from the value of

Rudra Logistics' godown in Ahmedabad, Gujarat supply.

4) Add: Charges for transport from Ahmedabad -

godown to the warehouse in Mumbai, (MH)

5) Add: Customs duty -

6) Add: Dock dues -

7) Add: Port charges -

8) Add: Hotel expenses 45,000 It would be treated as part of

9) Add: Travelling expenses 50,000 service and not in addition to

service he provides on his own

10) Add: Telephone expenses 2,000 account.

Value of Supply 5,97,000

Ü Yes, the answer would be different in second case.

Ü If lump sum amount of ₹ 13,00,000 is paid, then the value of supply shall be ₹ 13,00,000 and tax shall be

charged on value of supply since individual cost are not given.

15: Rule 34: Rate of exchange of currency, other than Indian rupees, for determination of value.

Q.25

Determine the Value of Taxable supply in independent cases:

1) BKC Ltd is a registered person located in Mumbai engaged in supply of auto spare units. PQR Ltd is a

foreign company located at New York places an order to BKC Ltd for delivery of 250 units of auto spare

parts to its branch office located at Pune. BKC ltd raises an invoice as on date of order i.e. 12.10.20XX the

cost of each unit of auto spare part was ₹175/-, the amount of consideration for such supply is received in

US $ as on 25.12.20XX from the foreign branch i.e. $ 690.25.

As on date of invoice the following rates are available:-

Exchange rate of RBI = ₹ 64.54 , CBIC rate = ₹ 63.94 & Actual bank rate = ₹ 64.45.

2) M/s ABC Ltd a business establishment in USA and has another establishment located in Mumbai (India)

for which an interior design work is required to be done for this it undertakes the service of Nirmitee

Interiors Pvt. ltd a registered person located at Mumbai. For the services rendered by Nirmitee

developers it raises an invoice as on date of provision of service i.e 02.03.20XX , the amount of

consideration for such supply is received in US Currency i.e. $ 1050 as on 13.05.20XX. As on date of

invoice the following rates are available:-

Exchange rate of RBI = ₹ 67.54, CBIC rate = ₹ 66.94 , GAAP rate = ₹ 67.84

Answer:-

1) Legal Provision:

Ü As per Rule 34 of CGST Rules 2017, The rate of exchange for determination of value of taxable goods

shall be the rate notified by the CBIC u/s 14 of the Customs Act 1962 for the date of time of supply of

such goods as per section 12 of the Act.

V’Smart Academy 6.20 CA Vishal Bhattad 09850850800