Page 18 - Ch15_Computation of GST

P. 18

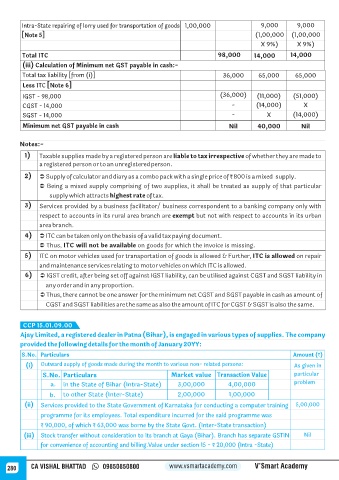

Intra-State repairing of lorry used for transportation of goods 1,00,000 9,000 9,000

[Note 5] (1,00,000 (1,00,000

X 9%) X 9%)

Total ITC 98,000 14,000 14,000

(iii) Calculation of Minimum net GST payable in cash:-

Total tax liability [from (i)] 36,000 65,000 65,000

Less ITC [Note 6]

IGST - 98,000 (36,000) (11,000) (51,000)

CGST - 14,000 - (14,000) X

SGST - 14,000 - X (14,000)

Minimum net GST payable in cash Nil 40,000 Nil

Notes:-

1) Taxable supplies made by a registered person are liable to tax irrespective of whether they are made to

a registered person or to an unregistered person.

2) Ü Supply of calculator and diary as a combo pack with a single price of ₹ 800 is a mixed supply.

Ü Being a mixed supply comprising of two supplies, it shall be treated as supply of that particular

supply which attracts highest rate of tax.

3) Services provided by a business facilitator/ business correspondent to a banking company only with

respect to accounts in its rural area branch are exempt but not with respect to accounts in its urban

area branch.

4) Ü ITC can be taken only on the basis of a valid tax paying document.

Ü Thus, ITC will not be available on goods for which the invoice is missing.

5) ITC on motor vehicles used for transportation of goods is allowed & Further, ITC is allowed on repair

and maintenance services relating to motor vehicles on which ITC is allowed.

6) Ü IGST credit, after being set off against IGST liability, can be utilised against CGST and SGST liability in

any order and in any proportion.

Ü Thus, there cannot be one answer for the minimum net CGST and SGST payable in cash as amount of

CGST and SGST liabilities are the same as also the amount of ITC for CGST & SGST is also the same.

CCP 15.01.09.00

Ajay Limited, a registered dealer in Patna (Bihar), is engaged in various types of supplies. The company

provided the following details for the month of January 20YY:

S.No. Particulars Amount (`)

(i) Outward supply of goods made during the month to various non- related persons: As given in

S.No. Particulars Market value Transaction Value particular

a. in the State of Bihar (Intra-State) 3,00,000 4,00,000 problem

b. to other State (Inter-State) 2,00,000 1,00,000

(ii) Services provided to the State Government of Karnataka for conducting a computer training 5,00,000

programme for its employees. Total expenditure incurred for the said programme was

₹ 90,000, of which ₹ 63,000 was borne by the State Govt. (Inter-State transaction)

(iii) Stock transfer without consideration to its branch at Gaya (Bihar). Branch has separate GSTIN Nil

for convenience of accounting and billing.Value under section 15 - ₹ 20,000 (Intra -State)

280 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy