Page 13 - Ch15_Computation of GST

P. 13

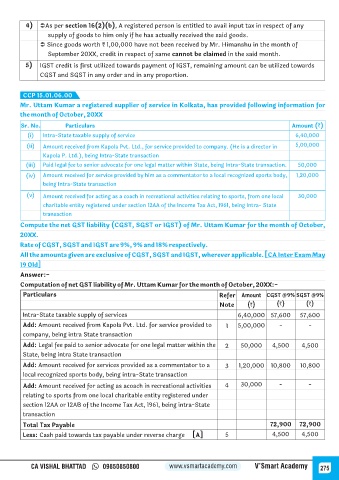

4) ÜAs per section 16(2)(b), A registered person is entitled to avail input tax in respect of any

supply of goods to him only if he has actually received the said goods.

Ü Since goods worth ₹ 1,00,000 have not been received by Mr. Himanshu in the month of

September 20XX, credit in respect of same cannot be claimed in the said month.

5) IGST credit is first utilized towards payment of IGST, remaining amount can be utilized towards

CGST and SGST in any order and in any proportion.

CCP 15.01.06.00

Mr. Uttam Kumar a registered supplier of service in Kolkata, has provided following information for

the month of October, 20XX

Sr. No. Particulars Amount (`)

(i) Intra-State taxable supply of service 6,40,000

(ii) Amount received from Kapola Pvt. Ltd., for service provided to company. (He is a director in 5,00,000

Kapola P. Ltd.), being Intra-State transaction

(iii) Paid legal fee to senior advocate for one legal matter within State, being Intra-State transaction. 50,000

(iv) Amount received for service provided by him as a commentator to a local recognized sports body, 1,20,000

being Intra-State transaction

(v) Amount received for acting as a coach in recreational activities relating to sports, from one local 30,000

charitable entity registered under section 12AA of the Income Tax Act, 1961, being Intra- State

transaction

Compute the net GST liability (CGST, SGST or IGST) of Mr. Uttam Kumar for the month of October,

20XX.

Rate of CGST, SGST and IGST are 9%, 9% and 18% respectively.

All the amounts given are exclusive of CGST, SGST and IGST, wherever applicable. [CA Inter Exam May

19 Old]

Answer:-

Computation of net GST liability of Mr. Uttam Kumar for the month of October, 20XX:-

Particulars Refer Amount CGST @9% SGST @9%

Note (`) (`) (`)

Intra-State taxable supply of services 6,40,000 57,600 57,600

Add: Amount received from Kapola Pvt. Ltd. for service provided to 1 5,00,000 - -

company, being intra State transaction

Add: Legal fee paid to senior advocate for one legal matter within the 2 50,000 4,500 4,500

State, being intra State transaction

Add: Amount received for services provided as a commentator to a 3 1,20,000 10,800 10,800

local recognized sports body, being intra-State transaction

Add: Amount received for acting as acoach in recreational activities 4 30,000 - -

relating to sports from one local charitable entity registered under

section 12AA or 12AB of the Income Tax Act, 1961, being intra-State

transaction

Total Tax Payable 72,900 72,900

Less: Cash paid towards tax payable under reverse charge [A] 5 4,500 4,500

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 275