Page 6 - Ch15_Computation of GST

P. 6

2 The company sold goods to X & Co. of Delhi on 6th January, 20XX with a condition 5,00,000

that interest @ 2% per month will be charged on invoice value if X & Co. failed to

make payment within 30 days of the delivery of the goods. Goods were delivered

and also the invoice was issued on 6th January, 20XX. X & Co. paid the

consideration for the goods on 20th February along with applicable interest.

3 The company sought legal consultancy services for it's business from A & 1,50,000

Advocates, a partnership firm of advocates situated at Bhuj, Gujarat.

4 The company ordered 3,000 packets of tools which are to be delivered by the 5,00,000

supplier of Delhi via 3 lots of 1,000 packets monthly. The supplier raised the invoice

for full quantity in February, 20XX and the last lot would be delivered in April, 20XX.

5 The company supplied 10,000 packets of tools to one of it's customer at ` 10/- per

packet in Gujarat in January, 20XX. Afterwards, the company re-values it at ` 9 per

packet in February, 20XX and the company issued credit note to the customer for

` 1 per packet.

The rate of GST is 9% CGST, 9% SGST and 18% IGST.

You are required to compute the actual net liability of GST to be paid in cash along with working notes

for the month of February, 20XX. [CA Inter Dec 21 Exam]

Answer:-

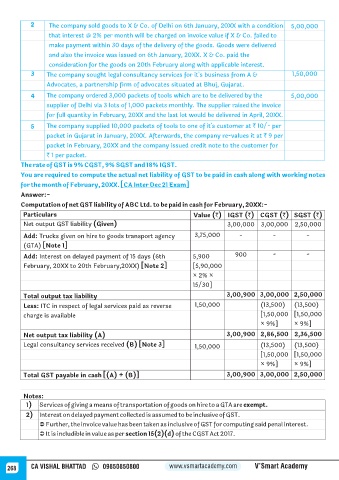

Computation of net GST liability of ABC Ltd. to be paid in cash for February, 20XX:-

Particulars Value (`) IGST (`) CGST (`) SGST (`)

Net output GST liability (Given) 3,00,000 3,00,000 2,50,000

Add: Trucks given on hire to goods transport agency 3,75,000 - - -

(GTA) [Note 1]

Add: Interest on delayed payment of 15 days (6th 5,900 900 - -

February, 20XX to 20th February,20XX) [Note 2] [5,90,000

× 2% ×

15/30]

Total output tax liability 3,00,900 3,00,000 2,50,000

Less: ITC in respect of legal services paid as reverse 1,50,000 (13,500) (13,500)

charge is available [1,50,000 [1,50,000

× 9%] × 9%]

Net output tax liability (A) 3,00,900 2,86,500 2,36,500

Legal consultancy services received (B) [Note 3] 1,50,000 (13,500) (13,500)

[1,50,000 [1,50,000

× 9%] × 9%]

Total GST payable in cash [(A) + (B)] 3,00,900 3,00,000 2,50,000

Notes:

1) Services of giving a means of transportation of goods on hire to a GTA are exempt.

2) Interest on delayed payment collected is assumed to be inclusive of GST.

Ü Further, the invoice value has been taken as inclusive of GST for computing said penal interest.

Ü It is includible in value as per section 15(2)(d) of the CGST Act 2017.

268 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy